Daily Update - March 23, 2023

Selected highlights of the day

By: Matthew Otto

Phreesia

has announced its financial results for the fiscal fourth quarter and fiscal year ended January 31, 2023. The company reported revenue of $76.6 million in the quarter, which is a 32% increase year-over-year, and revenue of $280.9 million in fiscal year 2023, a 32% increase year-over-year. The average number of healthcare services clients was 3,140 in the quarter, up 36% year-over-year, and 2,856 in fiscal year 2023, up 38% year-over-year. The net loss was $38.0 million in the quarter compared to $46.5 million prior year, and the net loss was $176.1 million in fiscal year 2023 as compared to $118.2 million in 2022. The company’s cash and cash equivalents as of January 31, 2023, was $176.7 million, down from $313.8 million as of January 31, 2022. On March 10, 2023, Silicon Valley Bank was closed by the California Department of Financial Protection and Innovation, which appointed the Federal Deposit Insurance Corporation as receiver, and on March 9, 2023, Phreesia transferred a substantial portion of its cash and cash equivalents from SVB to other financial institutions.

Phreesia has announced its fiscal year 2024 outlook, with expected revenue between $353 million and $356 million, representing a year-over-year growth of 26% to 27%. Adjusted EBITDA is expected to be between negative $65 million and negative $60 million for the same period. The company maintains its $500 million revenue target to be achieved by annualizing its highest-revenue quarter in fiscal year 2025 and expects to reach profitability in the same fiscal year.

- DA Davidson analyst Robert Simmons increased his price target from $28 to $30 with a Neutral rating.

- RBC Capital analyst Sean Dodge increased his price target from $26 to $33 with a Sector Perform rating.

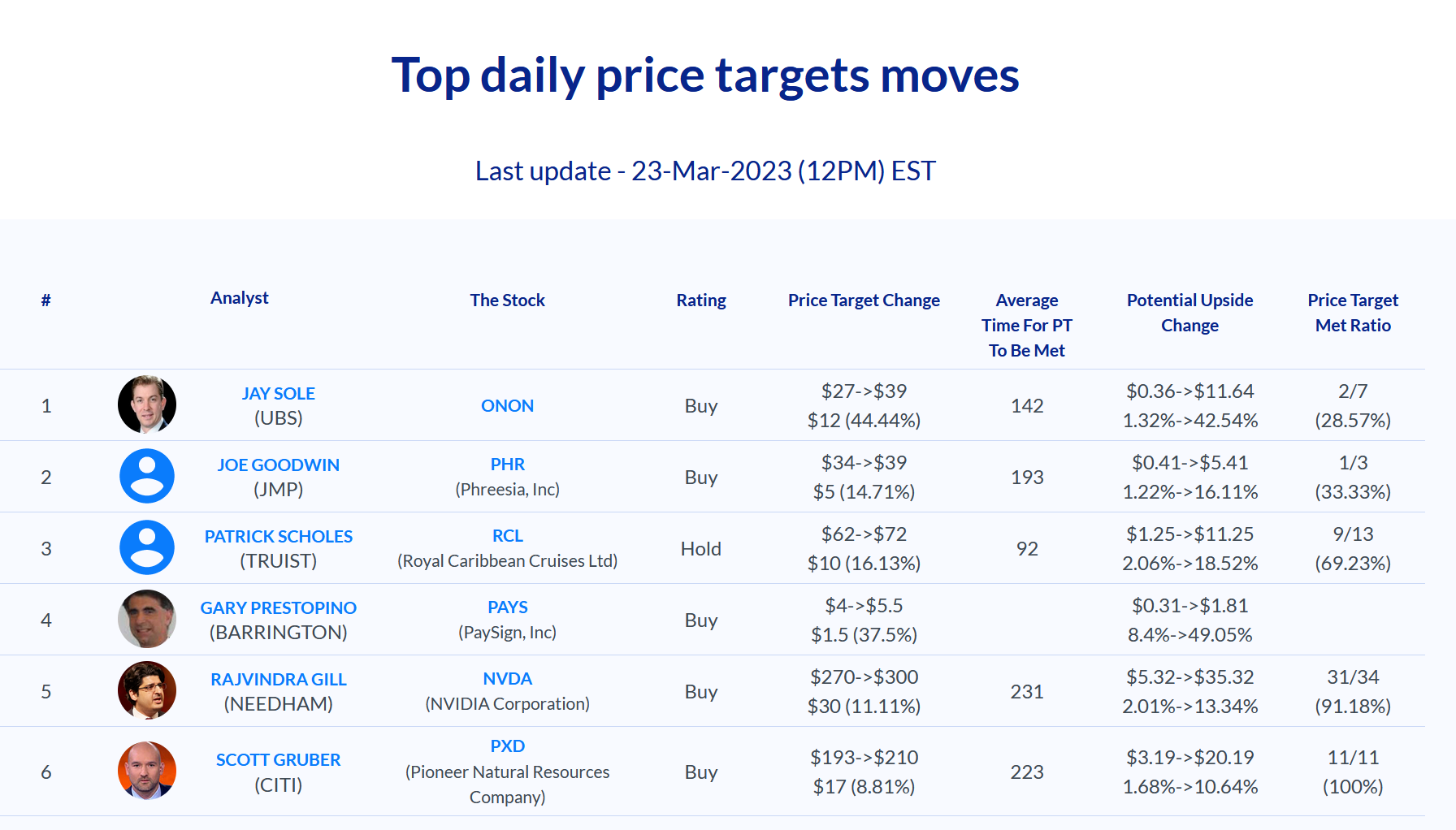

- JMP Securities analyst Joe Goodwin increased his price target from $145 to $220 with an Outperform rating.

- Needham analyst Ryan MacDonald reiterated a Buy rating and increased his price target from $64 to $40.

Coinbase Global

Has disclosed in a securities filing that it has received a “Wells Notice” from the US Securities and Exchange Commission (SEC) regarding a preliminary determination to recommend an enforcement action against the company. The notice relates to aspects of the company’s spot market, staking service Coinbase Earn. If crypto exchanges and tokens came under SEC oversight, the agency would have more powers to monitor trading, bring enforcement actions, and apply oversight to the token markets, potentially hindering the growth of the crypto industry in the US. Coinbase CEO Brian Armstrong tweeted that the company was “right on the law” and “confident in the facts” and welcomed the opportunity to present its case to a court.

- Needham analyst John Todaro reiterated a Buy rating on Coinbase Global and kept a price target of $73.

- Oppenheimer analyst Owen Lau downgraded Coinbase from Outperform to Perform.

Chewy

has announced its financial results for the fiscal fourth quarter and full year 2022 ended January 29, 2023. The highlights for the fourth quarter include net sales of $2.71 billion, which is a 13.4% increase year over year, gross margin of 28.1%, and adjusted EBITDA of $92.0 million, which is a 460 basis point expansion year over year. The company’s net income was $6.1 million, including share-based compensation expense of $50.2 million. The highlights for the fiscal year include net sales of $10.1 billion, which is a 13.6% increase year over year, gross margin of 28.0%, and adjusted EBITDA of $305.9 million, which is a 210 basis point expansion year over year. Chewy’s net income was $49.2 million, including share-based compensation expense of $163.2 million. Chewy CEO Sumit Singh stated that the company’s disciplined execution and widening ecosystem of offerings led to another year of market share gains in the pet category.

- Deutsche Bank analyst Lee Horowitz downgrades Chewy from Buy to Hold and lowers the price target from $41 to $35.

- Needham analyst Anna Andreeva reiterates Chewy with a Buy and maintains $55 price target.

- Barclays analyst Trevor Young maintains Chewy with Equal-Weight and lowers the price target from $35 to $33.

Darden Restaurants

Reported its financial results for the third quarter ended February 26, 2023, with total sales increasing 13.8% to $2.8 billion, driven by a blended same-restaurant sales increase of 11.7% and sales from 35 net new restaurants. Same-restaurant sales grew for all of its segments, including Olive Garden, LongHorn Steakhouse, Fine Dining, and Other Business. The company’s reported earnings also increased by 21.2% to $2.34.

Darden’s Board of Directors declared a quarterly cash dividend of $1.21 per share and the company repurchased approximately 0.87 million shares of its common stock for a total cost of approximately $124 million during the quarter.

Darden Restaurants updated its financial outlook for Fiscal 2023, with total sales expected to be between $10.45 billion and $10.5 billion, same-restaurant sales growth expected to be 6.5% to 7%, and new restaurant openings of approximately 55. The company also anticipates total capital spending of $550 to $575 million, total inflation of 7% to 7.5%, an effective tax rate of approximately 13%, diluted net earnings per share from continuing operations of $7.85 to $8.00, and approximately 123 million weighted average diluted shares outstanding.

- TD Cowen analyst Andrew Charles kept Darden with an Outperform and a $165 stock forecast.

- Citigroup analyst Jason Bazinet resumed AMC with a Sell rating and a $1.6 price target.

Ollie’s Bargain Outlet received a series of positive adjustments::

- Loop Capital Anthony Chukumba raised the price target from $42 to $58 with an Equal-Weight rating.

- Morgan Stanley Simeon Gutman increased the price target from $50 to $54 with an Equal-Weight rating.

- Goldman Sachs Kate McShane elevated the price target from $56 to $61 with a Neutral rating.

- Truist Securities Scot Ciccarelli maintains a Hold rating boosted the price target from $46 to $59.

KB Home

reported its financial results for Q1 2023, with total revenues of $1.38 billion and net income of $125.5 million. The company’s diluted earnings per share were $1.45 and book value per share reached $44.80. In addition, KB Home also announced a new stock repurchase authorization of $500 million. Net orders decreased by 49%, and net order value decreased by 53%. The company repurchased $1.5 Billionand its board authorized the additional repurchase of up to $500 million.

KB iis expecting housing revenues in the range of $5.20 billion to $5.90 billion.

- UBS analyst John Lovallo sustained KB Home with a Buy rating and lifted the price target from $45 to $48.

- RBC Capital analyst Mike Dahl maintains a Sector Perform rating and boosted the price target from $34 to $37.

Petco Health + Wellness Company

- Morgan Stanley analyst Simeon Gutman had an Equal-Weight rating and lowered his price target from $12 to $10

- Baird analyst Justin Kleber maintained an Outperform rating and downgraded his price target from $14 to $11.

- Needham analyst Anna Andreeva had not changed her Buy rating and lowered the price target from $20 to $12.

- RBC Capital analyst Steven Shemesh kept an Outperform rating and reduced his price target from $14 to $10.