Corporate Access and the Invisible Architecture of Sell-Side Analyst Performance

In March 2023, two analysts covering a large U.S. industrial company revised their earnings estimates weeks ahead of the broader consensus. The filings were public. The earnings call had not yet occurred. In their research notes, both cited recent “management meetings conducted during a non-deal roadshow.” No new information had been disclosed — but the timing advantage was real.

Episodes like this are not unusual in modern equity research.

Despite unprecedented transparency, sell-side analyst performance remains strikingly uneven. Selective disclosure is illegal. Earnings calls are transcribed and distributed globally within minutes. Regulatory filings are instantly searchable, and artificial intelligence can parse thousands of pages of disclosures faster than any human analyst.

Yet some analysts consistently lead estimate revisions, identify inflection points earlier, and shape market narratives — while others, armed with the same public data, largely follow consensus.

If information is broadly available to all participants at the same time, why does performance dispersion persist?

The answer lies not in information itself, but in the structure through which information flows. One of the least visible yet most influential components of that structure is corporate access — an institutionalized system of proximity that continues to shape how equity research is interpreted, valued, and rewarded.

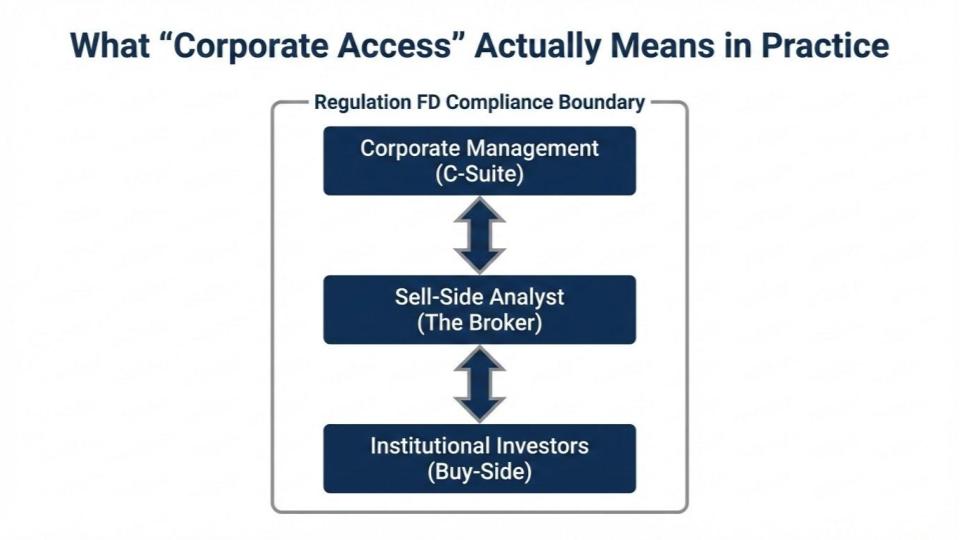

What “Corporate Access” Actually Means in Practice

Corporate access refers to broker-facilitated interactions between the management teams of public companies and institutional investors, coordinated through sell-side firms. These interactions typically involve the sector analyst, corporate investor-relations teams, and dedicated access coordinators.

In practice, access takes several high-touch forms:

- one-on-one meetings between senior executives and investors

- small group meetings hosted by brokers

- non-deal roadshows spanning multiple financial centers

- sector conferences featuring moderated management discussions

- operational site visits

All such interactions are subject to strict regulatory oversight. Regulation Fair Disclosure (Reg FD) prohibits the sharing of material non-public information with select investors. As a result, corporate access does not provide informational exclusivity in the legal sense.

The crucial distinction is this:

Corporate access is not about receiving new information — it is about interpreting public information through direct engagement.

It allows analysts and investors to evaluate how management communicates strategy, responds to scrutiny, and frames priorities — dimensions that do not appear in transcripts or spreadsheets.

From Privilege to Institution

Figure 1. Key regulatory milestones shaping modern equity research.

Source: Author’s illustration based on U.S. SEC Regulation FD (2000), the Global Research Analyst Settlement (2003), and MiFID II (2018).

Prior to 2000, analyst–management relationships were often informal and uneven. Selective disclosure was widespread, and proximity itself functioned as a competitive advantage.

That regime changed with the introduction of Regulation Fair Disclosure, which eliminated the private dissemination of material information. Yet while Reg FD altered what could be said, it did not eliminate interaction.

Regulation changed content, not contact.

The Global Research Analyst Settlement of 2003 further reshaped the sell-side by separating research from investment banking incentives. Corporate access survived — but increasingly as a structured, compliance-governed service rather than an informal relationship.

The most consequential shift arrived with the implementation of MiFID II in Europe in 2018. By unbundling research from trading commissions, MiFID II forced banks to assign explicit prices to services that had long been implicit.

In the post–MiFID II environment, banks began charging directly for access events, restricting participation for smaller asset managers, and closely tracking the return on management time. What had once functioned as relationship capital became economically visible.

The Modern Corporate Access Machine

Figure 2. Corporate access ecosystem (conceptual).

Figure 2. Corporate access ecosystem (conceptual).

Source: Author’s illustration based on Regulation FD disclosure boundaries.

Today, corporate access operates at scale.

Large global investment banks maintain dedicated corporate access teams — often numbering in the dozens — responsible for coordinating management engagement across regions. Industry research firms such as Coalition and Greenwich Associates have documented the magnitude of this activity, with major brokers facilitating tens of thousands of management meetings annually across conferences, roadshows, and one-on-one formats.

Flagship events illustrate the scale. At conferences such as the Morgan Stanley Global Healthcare Conference, agendas routinely feature more than 100 public companies presenting over several days to hundreds of institutional investors — a logistical undertaking rivaling large-scale corporate events.

Corporate access is no longer informal networking. It is institutional logistics, supported by technology platforms, compliance oversight, and internal performance tracking.

Access Is Not Evenly Distributed

Despite operating within a regime of public disclosure, corporate access introduces structural asymmetry.

Management time is scarce. Priority access typically flows to institutional clients that generate meaningful commission volume or pay explicitly for research services. Senior analysts with established reputations command disproportionate management attention, while junior analysts and smaller firms often face limited exposure.

Over time, access increasingly focuses on visibility.

This creates a reinforcing loop:

Access enhances reputation, and reputation attracts more access.

Even in transparent markets, proximity remains unevenly allocated.

How Corporate Access Shapes Analyst Performance

Figure 3. Reinforcing feedback loop in sell-side research performance.

Source: Author’s illustration.

Corporate access influences analyst performance through several identifiable channels.

Forecast interpretation

Academic research has examined the role of private interaction between management and sell-side analysts. A 2014 study published in the Journal of Accounting Research by Eugene Soltes found that such interactions were frequently associated with earlier estimate revisions, even when improvements in forecast accuracy were modest or mixed.

Direct engagement helps analysts interpret guidance, assess strategic emphasis, and evaluate managerial conviction — forms of “soft information” that resist codification.

Narrative timing

Markets respond not only to results but to shifts in narrative. Analysts with frequent management interaction are often better positioned to detect changes in tone or emphasis before those shifts manifest in reported earnings.

The advantage typically appears not in absolute correctness, but in timing — who moves first.

Professional outcomes

Institutional Investor and Extel analyst rankings play a central role in compensation and career progression. According to Institutional Investor’s published All-America Research Team methodology, analysts are evaluated not only on analytical insight and responsiveness, but also on their ability to provide access to company management.

As a result, access quality becomes intertwined with professional standing.

The Conflict at the Center of Sell-Side Research

The access ecosystem carries an inherent tension.

Because corporate participation is voluntary, analysts rely on management cooperation to host conferences and roadshows. Negative recommendations can jeopardize that cooperation, making independence professionally costly.

Critics have described this dynamic as “relationship research” — analysis shaped partly by the desire to preserve proximity.

The issue, however, is structural rather than personal. The incentive framework of modern equity research rewards both analytical judgment and access facilitation, embedding tension directly into the system.

Why Corporate Access Persists

The endurance of corporate access becomes clearer when compared with its alternatives.

Expert networks such as GLG, AlphaSights, and Tegus allow investors to speak with former employees, suppliers, and industry specialists — often providing deeper operational insight than management itself. Yet these platforms have not displaced corporate access.

The reason lies in accountability.

Experts offer perspective; management offers authority. Strategic intent, capital-allocation priorities, and long-term direction ultimately rest with executives who are legally responsible for outcomes.

Tone cannot be transcribed.

Conviction cannot be modeled.

Strategic intent remains qualitative.

Markets may price numbers — but investors still assess people.

Rethinking Analyst Performance

Understanding analyst performance, therefore, requires moving beyond static accuracy metrics.

Traditional measures capture whether estimates were correct. They do not capture when analysts moved, when narratives shifted early, or which analysts consistently led consensus changes.

Revision leadership, sequencing, and narrative divergence reveal positional advantage — where an analyst sits within the information network.

Evaluating performance at this level requires analytical infrastructure capable of measuring timing, clustering, and dispersion — not merely numerical outcomes.

Conclusion: The Invisible Architecture

Corporate access is neither a regulatory loophole nor a system of favoritism alone. It is an institutionalized structure of proximity that shapes how public information is interpreted, prioritized, and transmitted across financial markets.

In an era of abundant data and increasingly automated analysis, interpretive advantage remains deeply human — embedded in relationships, repetition, and closeness to corporate decision-makers.

To understand why some analysts consistently move first while others follow, one must look beyond models and forecasts to the invisible architecture beneath them — and to how close each analyst stands to the source.

References

Institutional Investor. (2024). All-America Research Team methodology. Institutional Investor.

https://www.institutionalinvestor.com

Soltes, E. F. (2014). Private interaction between firm management and sell-side analysts. Journal of Accounting Research, 52(1), 245–272.

https://doi.org/10.1111/1475-679X.12037

U.S. Securities and Exchange Commission. (2000). Selective disclosure and insider trading (Release Nos. 33-7881, 34-43154).

https://www.sec.gov/rules/final/33-7881.htm

Related Reading

- Sell-Side Equity Research in a Nutshell

- How Sell-Side Analysts Interact with Firms

- What Makes an Analyst Consistently Accurate?

🔍 See Real Analyst Track Records on AnaChart

AnaChart tracks 4,000+ Wall Street analysts — see their price target history, accuracy rate, and performance score for any stock.