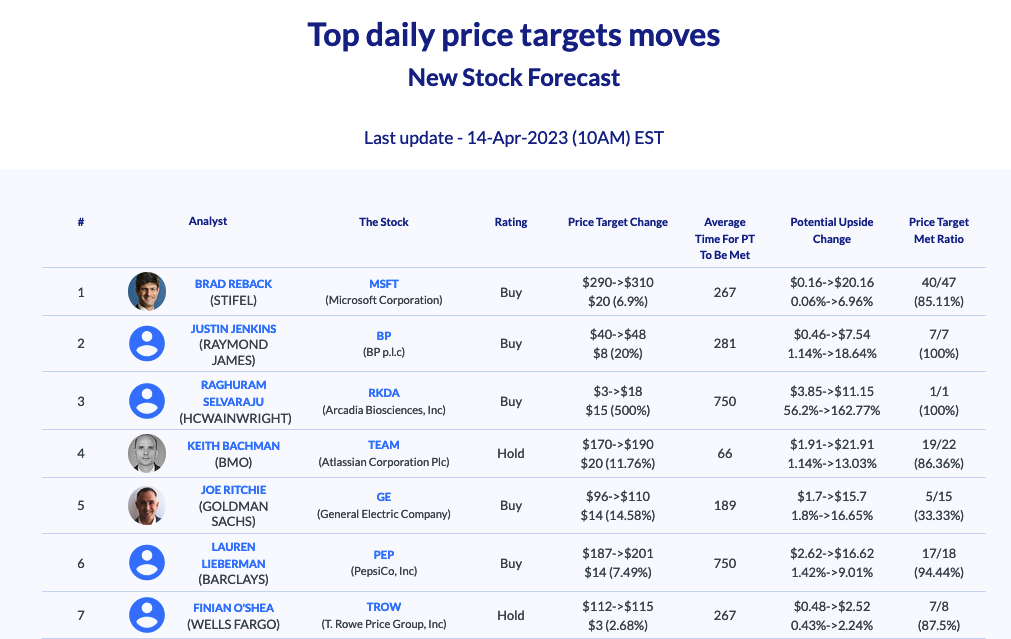

Daily Update - April 14, 2023

Selected highlights of the day:

By: Matthew Otto

Insurance claims on the rise

Progressive’s reported on Thursday that the company’s first-quarter combined ratio, which measures insurance company profitability, rose to 99% from 94.5% a year earlier. This increase indicates that the company is allocating more money to claims and operating expenses. The first-quarter net income was $0.75 per share, up from $0.52 per share a year ago. Net premiums written and net premiums earned also increased by 22% and 15%, respectively.

- Evercore ISI Group analyst David Motemaden maintains an Outperform rating but lowers the price target from $167 to $163.

- Credit Suisse analyst Andrew Kligerman reiterates a Neutral rating and maintains a price target of $143.

- BOFA Securities analyst Joshua Shanker maintains a Buy rating and raises the price target from $178 to $188.

- Barclays analyst Tracy Benguigui maintains an Underweight rating but lowers the price target from $121 to $118.

Out of the four analysts mentioned Andrew Kligerman had the most success with his bullish stance and giving proven stock forecasts in the last five years.

FDA might reject SRP-9001

Sarepta Therapeutics received headlines after a report by healthcare news website STAT stated that FDA reviewers had initially planned to reject the company’s application for approval of its gene therapy, SRP-9001, to treat Duchenne muscular dystrophy.

Duchenne muscular dystrophy (DMD) is a genetic disorder that affects muscle function and causes progressive muscle weakness and wasting. It primarily affects males, and symptoms usually start in early childhood. There is currently no cure for DMD, but there are treatments available that can help manage symptoms and improve quality of life. It affects approximately 1 in 3,500 to 5,000 male births worldwide.

- Despite the concern Mizuho analyst Uy Ear reiterates a Buy with a $160 price target.

- Morgan Stanley analyst Matthew Harrison kept an Overweight rating as well and a $183.00 price target.

ViewRay

Announced its preliminary financial results for the first quarter ended March 31, 2023. The company received 13 new orders for MRIdian systems totaling approximately $68 million, and the total backlog increased to approximately $411 million. The total revenue for the first quarter of 2023 was approximately $23 million, while the net loss for the quarter was approximately $29 million. Adjusted EBITDA was a loss of approximately $25 million. The company is exploring strategic alternatives to maximize shareholder value, including a corporate sale, merger, or business combination.

Outlook

The company is reducing its revenue guidance range to approximately zero to 15% growth for fiscal 2023 and updating its Adjusted EBITDA guidance range to a loss of $75 million to $85 million for fiscal 2023. The cash usage in the first quarter of 2023 was approximately $57 million, and the company anticipates that its cash balance of $86 million will get them into the first quarter of 2024.

Wall Street Reaction

- Oppenheimer analyst Suraj Kalia downgraded from Outperform to Perform and announced an $8 price target.

- Morgan Stanley analyst Cecilia Furlong maintained an Equal-Weight rating but lowered her price target from $5.5 to $2.

- BTIG analyst Marie Thibault downgraded ViewRay from Buy to Neutral

- Stifel analyst Rick Wise downgraded from Buy to Hold and lowered his price target from $7 to $1.75.

According to the chart on AnaChart, from the above, no analyst had success with predicting the stock price decline in the last five year

IMBI

On Wednesday,iMedia Brands has released its financial results for Q4 2022 and the full-year 2022, showing a 31% decrease in Q4 2022 net sales compared to Q4 2021 and a 1% decrease in full-year 2022 net sales compared to the previous year. The company has also completed a sale-leaseback transaction with Pontus Net Lease Advisors, and other supporting transactions that have reduced the company’s debt outstanding by $53 million. This has resulted in the company’s debt being approximately $123 million, approximately 41% lower than the company’s $207 million debt level at the end of Q1 2022. The company entered into a forbearance agreement with its senior lenders for a period of six months from the sale-leaseback date. Certain iMedia Directors and the company’s CEO have invested an aggregate of $300,000 in a Private Investment in Public Equity.

The management didn’t provide any outlook for the rest of the year.

Yesterday recommendations were:

- Craig-Hallum analyst Alex Fuhrman maintained a Buy rating and lowered the price target from $4 to $2.

- DA Davidson analyst Tom Forte kept with a Buy rating however he lowered the price target from $11 to $1.

- Lake Street analyst Mark Argento stayed with a Buy rating and lowered his price target from $2 to $1.

- B. Riley Securities analyst Eric Wold reiterated a Buy rating and dropped his price target from $3 to $2.

Delta Airlines receives feedback on yesterday’s news

- Morgan Stanley analyst Ravi Shanker maintains an Equal-Weight and raises the price target from $65 to $70.

- BOFA Securities analyst Andrew Didora maintains a Buy and lowers his price target from $43 to $40.