Daily Update - April 19, 2023

By: Matthew Otto

Selected highlights of the day:

As the season earning reports we deliver three stock that received attention in the news.

Johnson & Johnson

Reported a 5.6% increase in reported sales for the first quarter of 2023, with operational growth of 9.0% and adjusted operational growth of 7.6%. The company also reported a basic loss per share of ($0.03), due to a special one-time charge, but adjusted earnings per share (EPS) increased by 0.4% to $2.68. Johnson & Johnson is increasing its full-year guidance midpoints for adjusted operational sales and adjusted operational EPS.

For the full year 2023, Johnson & Johnson is increasing its adjusted operational sales midpoints by 1% to 4.5% – 5.5% and its adjusted operational EPS midpoint by 0.5% to $10.50 – $10.60. The company does not provide GAAP financial measures on a forward-looking basis due to the uncertainty of legal proceedings, unusual gains and losses, acquisition-related expenses, and purchase accounting fair value adjustments.

The CFO of Johnson & Johnson, Joe Wolk, has stated that the first step in the separation of the company’s consumer health division is imminent. The division, which includes major brands such as Tylenol and Band-Aid, will operate as a new company called Kenvue, under a plan announced in 2021. The separation will begin with an initial public offering (IPO). Johnson & Johnson reported better-than-expected earnings for the first quarter of 2023 and raised its earnings forecast for the full year. However, the company has also faced ongoing litigation over claims that talc in its baby powder products caused cancer. Johnson & Johnson had sought to move the litigation into bankruptcy court, but an appeals court judge rejected this in January. The company tried again in April and announced an $8.9 billion settlement agreement with some of the plaintiffs.

- Raymond James analyst Jayson Bedford maintains an Outperform but lowers his price target from $185 to $181.

- Atlantic Equities analyst Steve Chesney has a Neutral rating and drops his price target from $168 to $167.

- Morgan Stanley analyst Terence Flynn retains an Equal-Weight rating and upgrades his price target from $179 to $183.

Looking at AnaChart, Jayson Bedford has proven success with his placed in advance stock forecasts on the pharma giant since he started covering it in 2016 when the firm traded at half of the market value.

Netflix will be winding down its DVD-by-mail business

Which it had started around 25 years ago, stating that the service has been shrinking and it will not be able to continue to offer quality service. The company will ship the last discs on September 29. Netflix co-founder Marc Randolph described in his autobiography how he and co-founder Reed Hastings had flirted with the idea of challenging Blockbuster Video with mail-order VHS cassettes, but it would have cost too much. Instead, they landed on a more cost-effective proposition: DVDs sold and rented online. It was the first time Netflix’s gamble on an emerging technology allowed it to challenge an entrenched competitor. Rival Blockbuster filed for bankruptcy in 2010.

Netflix reported better-than-expected earnings for the first quarter of 2022, with earnings per share of $2.88 and revenue of $8.162 billion. However, the company’s growth forecast fell short of analysts’ expectations, indicating the challenges faced by the mature streaming service in its quest for continued growth. In addition to exploring new ways of generating revenue, such as its password crackdown and ad-supported service, Netflix is shifting the wider launch of its password crackdown plan to the second quarter to make improvements, delaying some financial benefits. As competition in the streaming industry continues to intensify, Netflix’s earnings results are closely watched as a bellwether for the sector.

The streaming video service added 1.75 million net new subscribers in the quarter, about 500,000 less than analysts had predicted. Revenue and earnings for the quarter came roughly in line with the average analyst estimates. It posted revenue of $8.17 billion, up 3.7%, with profits of $2.88 a share. Netflix’s forecast for full-year free cash flow is at least $3.5 billion, from a previous forecast of at least $3 billion.

- Piper Sandler analyst Thomas Champion maintained a Neutral rating and raised his price target from $325 to $350.

- JP Morgan analyst Doug Anmuth keeps an Overweight rating but lowered the price target from $390 to $380.

- Deutsche Bank analyst Bryan Kraft has a Buy rating and raised his price target from $400 to $410.

- UBS analyst John Hodulik upgraded Netflix from Neutral to Buy and raised the price target from $350 to $390.

- Jefferies analyst Andrew Uerkwitz maintains a Buy rating but lowers his price target from $415 to $405.

- Pivotal Research analyst Jeffrey Wlodarczak maintains a Buy rating and raises his price target from $400 to $425.

Half of the current price target on NFLX are below the stock price and half are.

Intuitive Surgical

Announced financial results for the quarter ended March 31, 2023. The company’s Q1 highlights include 26% YoY growth in worldwide da Vinci procedures, placing 312 da Vinci Surgical Systems, 12% YoY growth in the da Vinci Surgical System installed base to 7,779 systems, and Q1 2023 revenue of $1.7 billion, a 14% YoY increase. However, GAAP net income attributable to Intuitive in Q1 2023 was $355 million, or $1.00 per diluted share, compared to $366 million, or $1.00 per diluted share, in the same period last year.

Intuitive reported better-than-expected earnings for the first quarter of 2023, with adjusted earnings per share of $1.23 beating the consensus estimate of $1.20 per share. Additionally, the company’s revenue of $1.70 billion came in ahead of expectations, compared to estimates of $1.59 billion. The 14% year-over-year revenue growth was driven by growth in da Vinci procedure volume, partially offset by foreign currency impacts.

- Stifel analyst Matthew Sheerin affirms a Buy rating and raises the price target from $285 to $315.

- Deutsche Bank analyst Imron Zafar maintains a Hold rating while reducing the price target from $245 to $290.

- Piper Sandler analyst Richard Repetto reiterates an Overweight rating and increases the price target from $265 to $315.

- BTIG analyst Ryan Zimmerman sustains a Buy rating and elevates the price target from $284 to $313.

- Evercore ISI Group analyst Vijay Kumar holds an In-Line rating and upgrades the price target from $240 to $270.

- JP Morgan analyst Robbie Marcus maintains an Overweight rating and lifts the price target from $250 to $335.

- RBC Capital analyst Shagun Singh keeps an Outperform rating and boosts the price target from $305 to $309.

- Morgan Stanley analyst Cecilia Furlong retains an Equal-Weight rating while raising the price target from $265 to $285.

- Truist Securities analyst Richard Newitter preserves a Buy rating and raises the price target from $300 to $325.

- B of A Securities analyst Travis Steed maintains a Buy rating and raises the price target from $300 to $315.

- Mizuho analyst Anthony Petrone maintains a Neutral rating while increasing the price target from $250 to $300.

- Wells Fargo analyst Larry Biegelsen upholds an Overweight rating and lifts the price target from $289 to $310.

- Raymond James analyst Jason Bednar maintains an Outperform rating and increases the price target from $270 to $323.

- Citigroup analyst Joanne Wuensch maintains a Buy rating and raises the price target from $305 to $317.

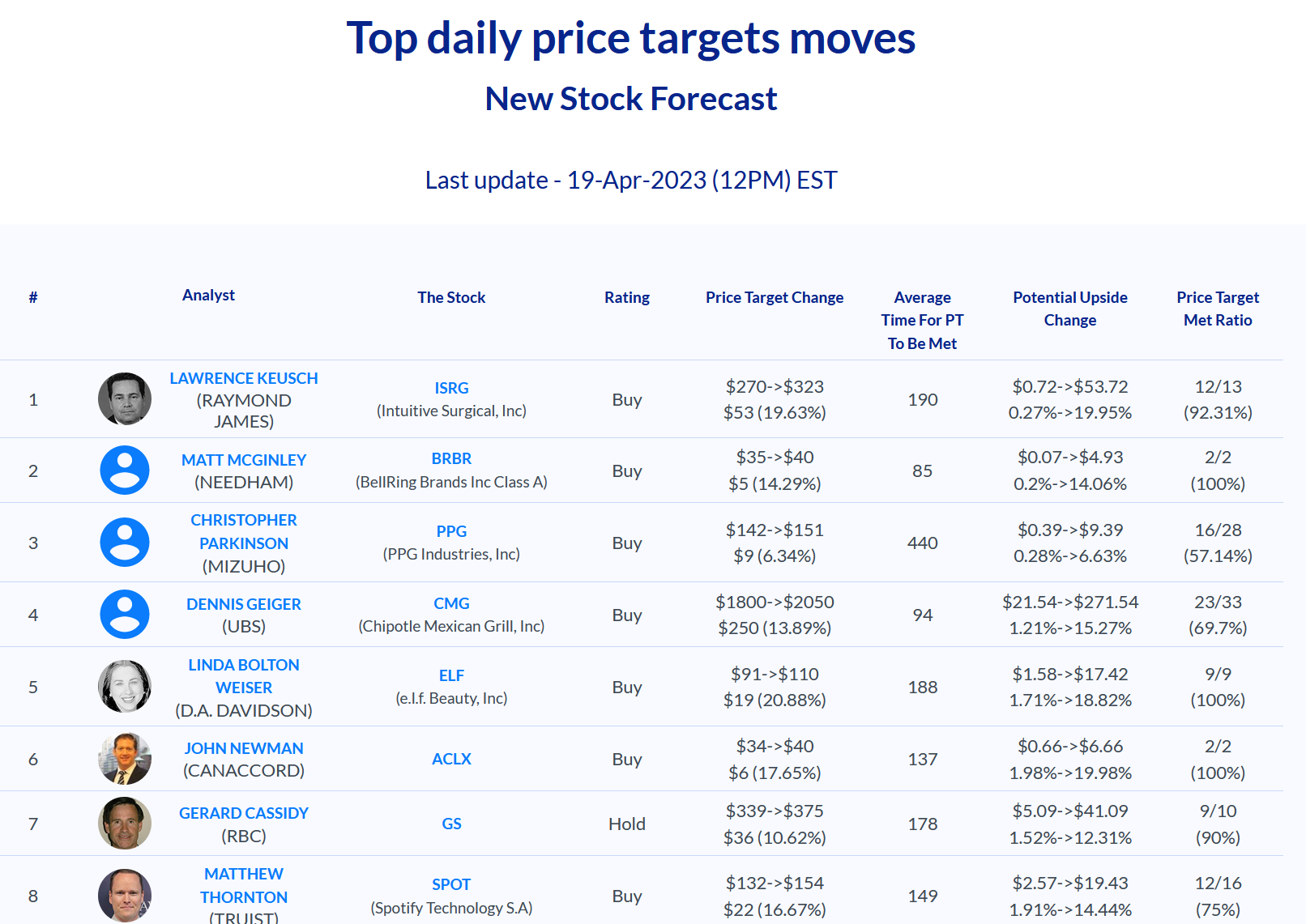

Shown below are the top daily price targets moves for April 19 2023