Daily Update - April 4, 2023

Selected highlights of the day:

By: Matthew Otto

Ascendis hits a roadblock with FDA

Ascendis Pharma announced that the U.S. Food & Drug Administration (FDA) has identified deficiencies in the Company’s New Drug Application (NDA) for TransCon PTH (palopegteriparatide) in hypoparathyroidism that precludes them from holding further discussions about labeling and post-marketing requirements/commitments. PTH helps regulate the levels of calcium and phosphate in the body, and its deficiency can lead to a range of symptoms such as muscle cramps, weakness, seizures, and bone disorders. The deficiencies were not disclosed in the letter, and the FDA stated that this does not reflect their final regulatory decision on the Company’s application

- Morgan Stanley analyst Vikram Purohit downgrades Ascendis Pharma from Overweight to Equal-Weight and lowers his price target from $151 to $108.

- B of A Securities analyst Tazeen Ahmad keeps Ascendis with a Buy and lowers the price target from $132 to $92.

- Credit Suisse analyst Tiago Fauth downgrades Ascendis from Outperform to Neutral.

- Goldman Sachs analyst Paul Choi sets a price target at $155.

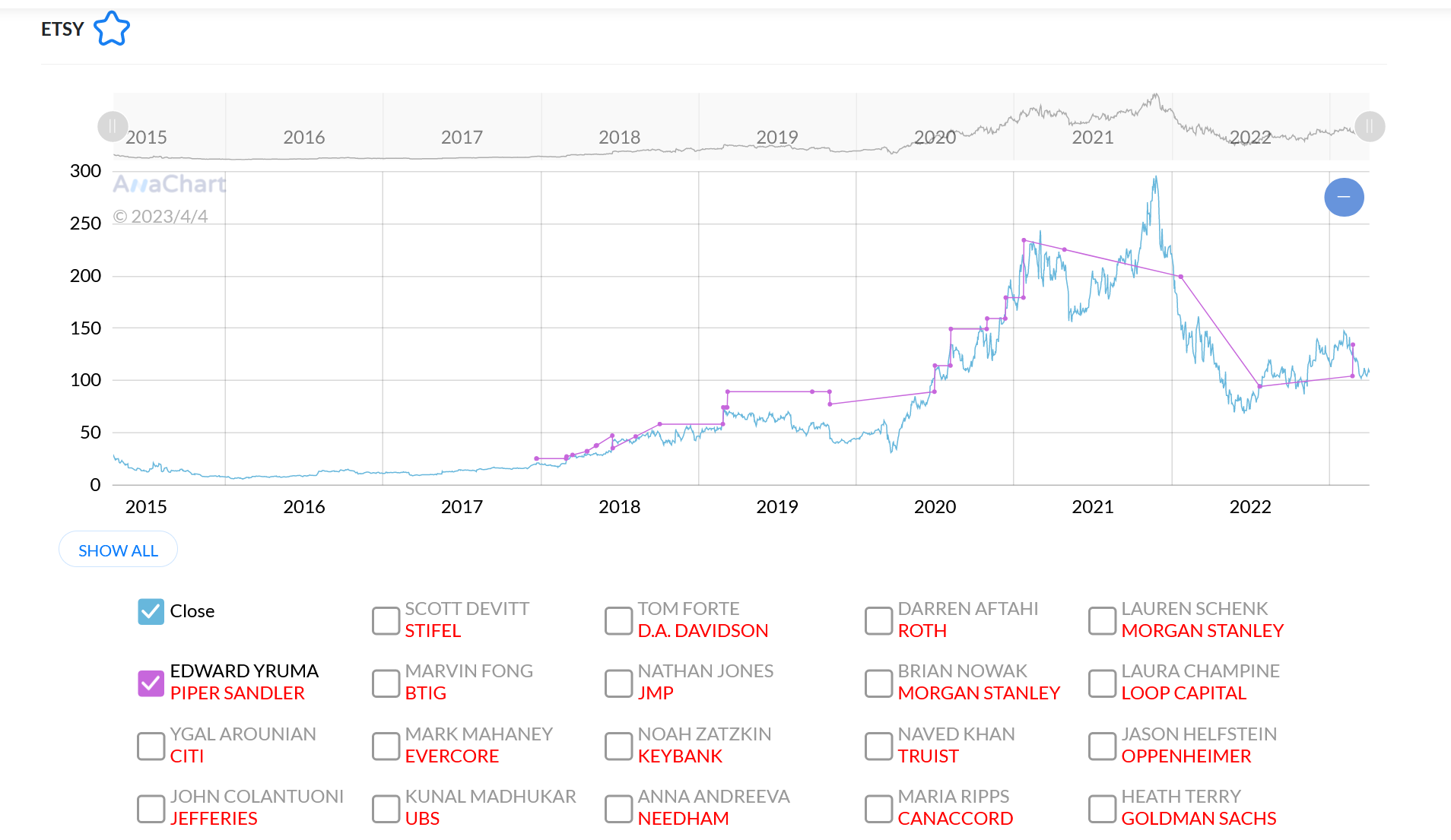

Etsy Receives positive feedback as the Gen Z popular choice

Piper Sandler analyst Edward Yruma has upgraded Etsy to Overweight from Neutral and increased his 12-month price target to $140 from $135. Cited on Barron’s Yruma mentioned that Etsy’s growth since the pandemic due to its popularity among the younger generation as a reason for the upgrade. He notes that Etsy’s focus on personalization of products and the sheer amount of items available for purchase on the app sets it apart from its competitors. While Yruma does recognize economic challenges that could impact the company in the near term, he is still confident in its growth opportunities over the long-term and sees the current stock valuation as a perfect buying opportunity. According to FactSet, Etsy’s current enterprise value to earnings before interest, taxes, depreciation, and amortization (EV/Ebitda) of 32.3 times is below its five-year average of 54.2 times.

As shown in the picture below Yruma had successfully predicted the stock rise in 2018 to 2021 but failed to predict the stock decline in the last two years.

Oncternal drops zilovertamab

Oncternal Therapeutics has announced a strategic reprioritization to focus on the development of two pipeline assets, ONCT-808 and ONCT-534, while closing the Phase 3 study and the Phase 1/2 study of zilovertamab, a monoclonal antibody therapeutics for the treatment of various types of cancer, including mantle cell lymphoma (MCL) and chronic lymphocytic leukemia (CLL), in combination with ibrutinib. The decision was based on the rapidly changing commercial landscape for Bruton’s tyrosine kinase inhibitors (BTK inhibitors), which made the continued development of zilovertamab with ibrutinib an unviable commercial opportunity.

The announcement was not taken well by wall street.

- Brookline Capital analyst Kemp Dolliver downgraded from Buy to Hold.

- Cantor Fitzgerald analyst Li Watsek maintained an Overweight rating but lowered the price target from $4 to $1.3.

- HC Wainwright & Co. analyst Raghuram Selvaraju downgraded from Buy to Neutral.

- Oppenheimer analyst Hartaj Singh downgraded from Outperform to Perform.

- Maxim Group analyst Naureen Quibria downgraded to Hold.

Norfolk Southern to announce Q1 2023 earnings results on April 26

Earlier this week the U.S. Justice Department sued Norfolk Southern seeking penalties and injunctive relief for the unlawful discharge of pollutants under the Clean Water Act and an order addressing liability for past and future costs. The lawsuit was filed after the Norfolk-operated train derailment on February 3 of 38 cars including 11 carrying hazardous materials in the village of East Palestine caused cars carrying toxic vinyl chloride and other hazardous chemicals to spill and catch fire.

- Wolfe Research analyst Scott Group has Norfolk price target to $251.

- Morgan Stanley analyst Ravi Shanker upgrades Norfolk from Underweight to Equal-Weight and sets a price target of $177.

Ali Baba keeps receiving affection

- Benchmark analyst Fawne Jiang reiterates Buy rating and maintains $180 price target.

- HSBC analyst Charlene Liu maintains Buy rating and raises the price target from $138 to $143.

Expressed concerns for Boing

Northcoast Research analyst Chris Olin downgraded the aviation firm from Neutral to Sell, citing expected changes to commercial aircraft production, resetting of consensus forecasts, and volume headwinds ahead for Boeing in the current quarter after communicating with contacts in the sector. Olin also announced a $180 price target for the company.

Burlington Stores get upgraded

- Loop Capital analyst Laura Champine upgrades from Hold to Buy and raises the price target from $220 to $225, citing the likelihood of market share gains for the company due to improved values and brands in stores. Champine have proved herself in the last five years with her stock forecasts both when the stock moved up and down

- JP Morgan analyst Matthew Boss maintains Burlington Stores with an Overweight rating and raises the price target from $240 to $245. Boss has success predicting while the stock was going up but not down.