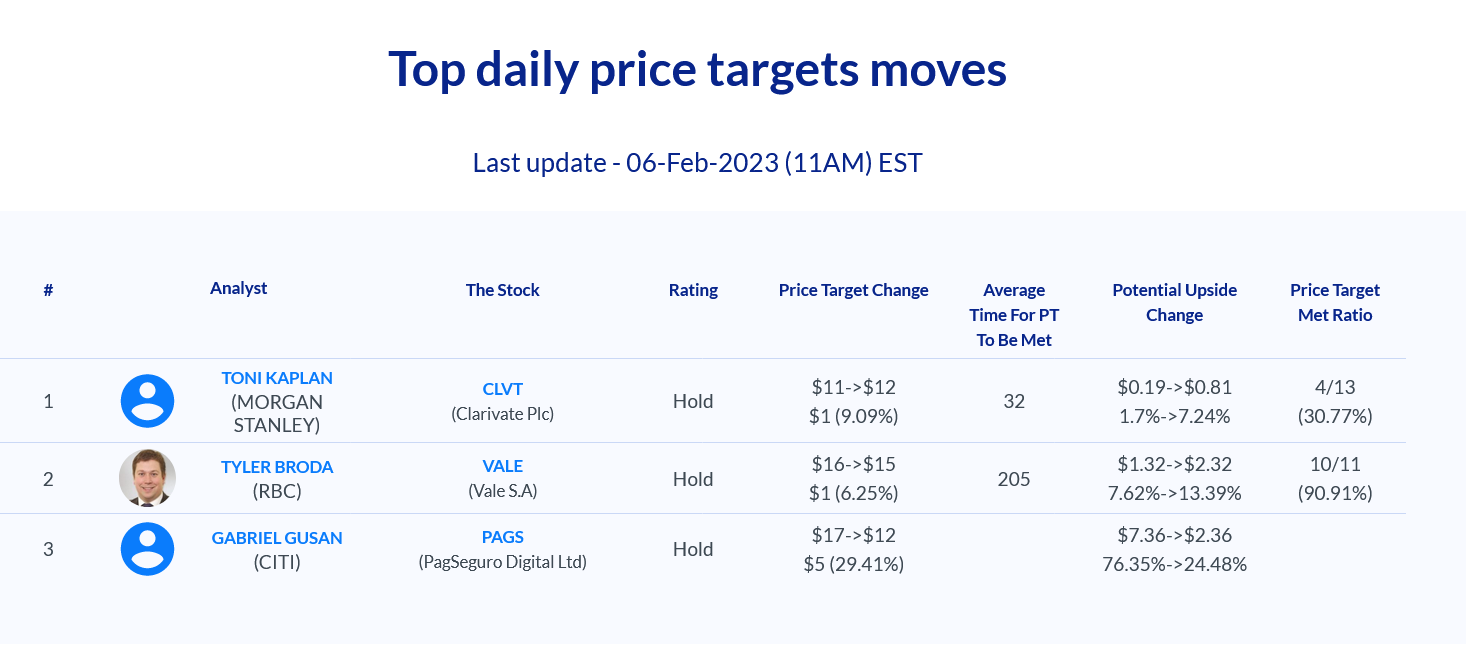

Daily Update - February 6, 2023

Selected highlights of the day

By: Matthew Otto

Evercore removes Apple from its targeted group

- Evercore ISI Group analyst Amit Daryanani reiterated a $190 price target while removing it from the Tactical Outperform list.

Ives continues to show confidence in Tesla

- Wedbush analyst Daniel Ives is confident in Tesla’s stock and has upped the price target from $200 to $225.

Consumers now have an opportunity to bring home a 2022 Model Y Performance edition with low mileage for far below retail, thanks not only reduced pricing but also potential savings of up to $7,500 through Federal tax credit qualification.

SAIA

In the fourth quarter of 2022, Saia reported a 6.3% increase in revenue to $655.7 million and an 85.9% operating ratio compared with 84.2%. However, the company’s diluted earnings per share fell from 2Q 2021’s figure of $2.76 down to $2. Compared with last year, revenue increased by 22.0% while operating income grew 40.4%, and LTL shipments per workday decreasing only slightly at 0.8%. Notable improvements included a 2.3% decrease in the company’s operating ratio from 85.4% down to 83.1%; as well as 19-21% jumps in both rates of LTL revenue per hundredweight and shipment rate ($351).

- Goldman Sachs analyst Jordan Alliger has maintained his assessment of Saia as Neutral while increasing their price target from $232 to $262.

- Analyst Jonathan Chappell of Evercore ISI Group adjusted his price target upward from $248 to $298 while keeping a rating of In-Line.

- Jack Atkins of Stephens pushed up his price target from $265 to $365 and maintaining an Overweight outlook.

- Whist upgrading his initial target from $229 to $283, Cowen & Co. analyst Jason Seidl expressed a Market Perform sentiment towards Saia.

- Wells Fargo analyst Allison Poliniak Cusic increased her suggested price target from $242 to $330, with a maintained Overweight.

- Benchmark analyst Christopher Kuhn raised his rating from Buy and shifted his price target from $230 up to $320.

- Credit Suisse’s analyst Ariel Rosa upped his proposed targets from $288 up to $312.

LyondellBasell released its 2022 earnings report

Net income was $353 million, and $427 million excluding identified items. Diluted earnings per share was reported at $1.07 and $1.29 excluding identified items. Additionally, EBITDA was reported at $792 million and $865 million excluding any identified items.

Cash from operating activities also saw positive uplift in the fourth quarter; reaching a peak of 1.6 billion USD, largely due to efforts in advancing their technologies around plastic waste sorting inputted into sophisticated recycling functions such as their MoReTec technology for their commercial recycling plants. Efforts towards optimizing renewable energy sources have been noted with the announcement of a new 2030 greenhouse gas emissions target relative to 2020 levels, and a further aim to reduce associated Scope 3 emissions in accordance with science-based advice and standards outlined by the EcoV planetary system.

Net income was recorded at $3.9 billion, amounting to $11.81 per share and excluding identified items it reached 4.1 billion and 12.46 per share respectively. This is further attested by their EBITDA standing at 6.3 billion, again increasing when excluding identified items to 6.5 billion, indicating attractive relative returns as proven through a 16 percent return on invested capital in 2022. Overall, the firm was able to deliver an aggregate of $6.1 billion in cash flow from operating activities during this period.

Wall Street Action

- Deutsche Bank analyst David Begleiter has maintained his Hold rating on LyondellBasell and raised the price target from $85 to $100.

- BAML Securities analyst Steve Byrne raised the price target from $77 to $90 yet maintained an Underperform rating.

- Wells Fargo analyst Michael Sison changed his target from $97 to $109, keeping an Overweight rating.

- Mizuho analyst Christopher Parkinson upgraded his price target from $89 to $91 and maintaining a Neutral outlook.

- Credit Suisse analyst Matt Skowronski increased his price projection for the company to $109, simultaneously upgrading it to Outperform.

- Keybanc’s Aleksey Yefremov increased his target from $83 to $85 while still maintaining an Underweight position.

Regeneron Pharmaceuticals reported a better-than-expected fourth quarter profit

Regeneron Pharmaceuticals’ blockbuster eye drug Eylea registered total sales of $9.65 billion in 2022. However, in the fourth quarter of 2022, total revenues for Eylea decreased to $3.41 billion due to sustained competition from Roche’s Vabysmo, which was approved last year.

When comparing full year 2022 to 2021, the revenues for Eylea decreased by 24%, bringing it down to $12.17 billion. However, when excluding revenues from REGEN-COV and Ronapreve an overall increase of 17% was observed across the board. This suggests that Regeneron Pharmaceuticals is experiencing growth in other areas of their business, such as with their eczema drug Dupixent, which is in strong demand.

It’s worth noting that the slump in U.S. based fourth quarter 2022 Eylea sales highlights issues related to market competition currently being posed for the drug.

- RBC Capital analyst Brian Abrahams has lowered his price target for Regeneron from $789 to $787 and maintained a Sector Perform rating.

- Baird analyst Brian Skorney adjusted his price target from $670 to $756 while maintaining a Neutral stance.

- Morgan Stanley analyst Matthew Harrison revised his price target from $873 to $883 and retained an Overweight status.

- SVB Leerink analyst David Risinger raised the price target from $770 to $884 while sustaining his Market Perform opinion.

Church & Dwight reported its fourth quarter and full year financial results for 2022.

In terms of the fourth quarter, net sales grew by 4.9%, with domestic growth of 7.6% and international weakening by 4.4%. SPD also weakened by 1.3%, meaning overall organic sales increased by 0.4%. This included a spike in international organic sales of 1.3%. Operating income plummeted 212.5%, yet was up 23.9% when adjusted for other factors.

Nnet sales rose 3.6%; further boosted by organics growing to an impressive 1.4%. Alongside this was Reported EPS rating at a level of $1.68. Finally cash flow generated $885 million.

- Steve Powers of Deutsche Bank, has maintained his Buy recommendation while increasing the price target to $92 from $91.

- Mark Astrachan of Stifel moved his price target from $79 to $85 while still maintaining a Hold rating.

- Dara Mohsenian at Morgan Stanley updated her price target to $92 and retained her Overweight recommendation.

- Edward Lewis from Atlantic Equities increased his Underweight rating to Neutral, with a price target of $80.

RH

Restoration Hardware got wall street attention as:

- Wedbush analyst Seth Basham had set a Neutral and raised his price target of $335 from $270.

- Citigroup’s Steven Zaccone maintained a Buy on RH while ramping up his price target from $305 to $380.

- Telsey Advisory Group’s Cristina Fernandez had a Market Perform and $330 per share target price.