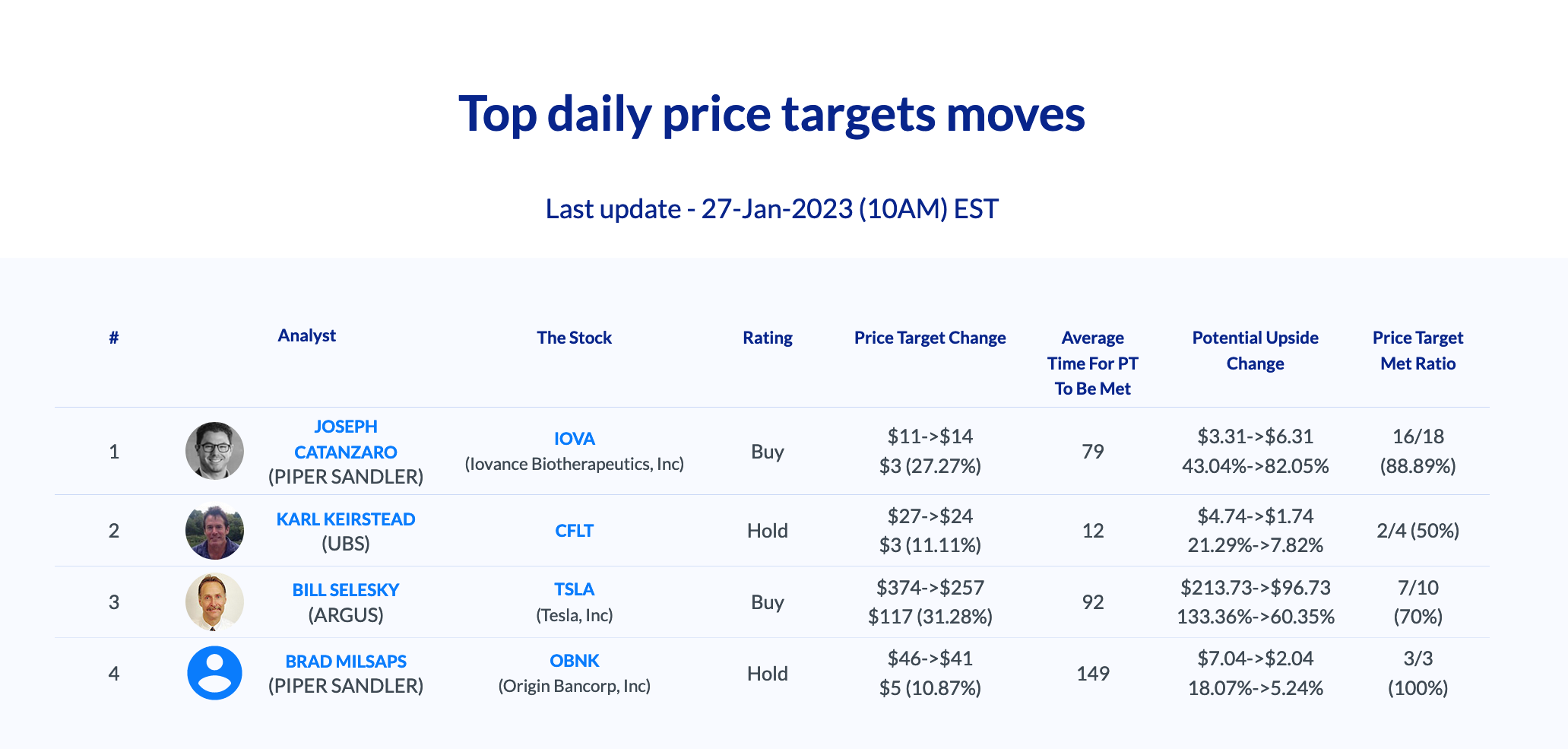

Daily Update - Jan 27, 2023

Selected highlights of the day

By: Matthew Otto

INTL

Intel’s earnings for the fourth quarter fell short of analyst expectations on Thursday, with the chip maker reporting adjusted earnings per share of only 10 cents compared to the consensus estimate of 21 cents, as stated by FactSet. Intel revenue was lower than expected at $14 billion versus the anticipated $14.49 billion. And the company revealed its outlook for their March quarter is far below expectations, coming in at a range of between $10.5 billion to $11.5 billion versus the consensus figure of $13.93 billion. To try and explain its disappointing numbers, Intel cited its weakest region was China in relation to initial expectations for this period.

- Aaron Rakers of Wells Fargo covers Intel and has downgraded it to an Equal Weight, with a price target decrease from $32 to $26.

- Matt Bryson of Wedbush has maintained an Underperform rating on Intel and lowered the price target from $23 to $20.

- Hans Mosesmann of Rosenblatt has decreased the price target of Intel from $20 to $17 while maintaining a Sell.

- Chris Caso at Credit Suisse kept Neutral on Intel with their price target dipping from $28 to $25.

- Blayne Curtis at Barclays maintained their Equal Weight but decreased the price target from $30 to $27.

- Harlan Sur of JP Morgan maintained his Underweight stance but reduced Intel’s price target from $32 to $28.

- Ross Seymore of Deutsche Bank reduced his Hold rating’s price target for Intel from $32 to $28.

AXFA

Axalta announced their fourth quarter and full year 2022 financial results. The details revealed a year over year volume growth of 2.4%, with price-mix growth of 11.7%. Income from operations was $109.8 million, representing a 15.9% increase compared to Q4 2021, while adjusted EBIT was $147.2 million, up 21.7%. These increases show a successful earnings hopeful as it transitions into 2023.

To round out the quarterly results, Axalta achieved Diluted EPS of $0.20 compared with Q4 2021’s rate of $0.23, with adjusted diluted EPS reflecting a huge jump to $0.38 up from Q4’s $0.30 result, proving effective management and strategic decision making in both net leverage and maturing loans from 2022 to December 2029.

- Yesterday Credit Suisse analyst John Roberts maintained his Underperform rating while raising the price target from $20 to $24.

- today, Baird analyst Ghansham Panjabi held his Outperform rating raising the price target from $30 to $35.

- Mizuho’s Christopher Parkinson maintained his Buy rating while raising his price target from $30 to $31.

- Keybanc analyst Aleksey Yefremov raised the price target from $30 to $32 while holding to an Overweight opinion.

- Barclays’ Brandon Oglenski maintained an Equal-Weight rating but increased his stock forecast from $50 to $54.

SAP looking to sell XM

Dropped news in its recent earnings report that it has retained Morgan Stanley as a financial advisor to assist with selling its majority stake in the customer experience management company Qualtrics. This comes two years after purchasing Qualtrics for $8 billion in cash in 2019.

The German software giant initially sold a minority stake in an IPO for Qualtrics at $30 per share, however this stake is currently valued at only $11.21 due to its rocky path since entering the public market.

Currently, SAP owns about 70% of Qualtrics stock, or 61% when accounting for dilution. The current market cap for all Qualtrics shares stands at $6.6 billion, nearly 2x less than what BMW paid just two years ago due to an overhang on valuation linked to leaving SAP in control of such a large share.

- yesterday Barclays analyst Raimo Lenschow maintained an Equal-Weight rating on Qualtrics and increased the price target from $11 to $15.

- Today, analyst Keith Bachman from BMO Capital raised his recommendation to an Outperform along with increasing his price target from $13 up to $17.

- Brian Peterson at Raymond James kept his recommendation a Market Outperform but raised the price point from its prior level of $14 to $17.

- Joey Marincek from JMP Securities announced a Market Outperform rating and lowered the price target of $28 down to $20.

Vir Biotechnology

Announced the retirement of George Scangos, Ph.D., Founder and longtime CEO of the company, who is succeeded by Marianne De Backer, MSc, Ph.D., MBA. Dr. De Backer brings to this senior role a background in leadership, which has occurred on a global scale. With over two decades experience as one accountable in strategic healthcare alliances coupled with extensive technology license relations further augmented by billions of dollars in merger and acquisition deals. Before joining Bayer Pharmaceuticals, Dr. De Backer had spent two decades at the Johnson & Johnson.

- SVB Leerink’s Roanna Ruiz has attributed an Outperform rating to Vir but lowered the price target from $45 to $43.

- Michael Ulz at Morgan Stanley has upgraded Vir from Underweight to Equal Weight and raised the price target from $18 to $30.

Visa

Reported financial performance for the quarter, earning $1.99 per share from their $7.9 billion in revenue according to Generally Accepted Accounting Principles (GAAP). After adjusting for $341 million in litigation expenses and a $106 million loss from equity investments, their profits came to $4.6 billion, or a substantial $2.18 per share, surpassing the analysts’ revised estimate of $2.01 per share with revenue of $7.7 billion.

Revenue grew year-over-year by 12%. This included a 22% increase in cardholder spending abroad and a 10% rise in processed transactions through Visa’s payment system. Profits just beyond GAAP guidelines similarly climbed by 17%.

What’s more, Visa showed its appreciation toward its shareholders through buybacks and dividends during the execution of its fourth quarter—well over their estimated return of roughly $4 billion. Alfred Kelly concluded his time as chief executive at Visa shortly afterwards and handed off leadership duties to Ryan McInerney as he assumed top spot this past February 1st.

- JP Morgan analyst Tien-Tsin Huang gives Visa an Overweight rating and increases the price target to $265.

- BMO Capital analyst James Fotheringham gives an Outperform rating to Visa and raises the price target from $249 to $253.

- Wells Fargo analyst Donald Fandetti also gives Visa an Overweight rating with an increase in price target from $250 to $265.

- Raymond James analyst John Davis is maintaining the Outperform rating and raising his price target from $261 to $281.

- Credit Suisse analyst Moshe Orenbuch is keeping an Outperform rating and upgrades his price target from $245 to $250.

Mastercard

Has reported better-than-expected earnings for the fourth quarter as well, arising from signs of a healthy consumer and China’s resumption of services.

The company saw net revenue rise to $5.8 billion on a currency neutral basis, with earnings per share of $2.65 surpassing the consensus estimate of $2.57.

Multiple stock analysts have provided their assessments in response to the news, offering modifications to their price targets and in some cases maintaining their ratings accordingly.

- Morgan Stanley analyst James Faucette retains his Overweight rating for Mastercard and is raising his price target from $437 up to $438.

- Susquehanna analyst James Friedman increased his target price from $405 to $433 and maintaining his Positive rating.

- Raymond James analyst John Davis has an Outperform rating with a target price lifted up from $406 to $450.

- BMO Capital analyst James Fotheringham is sustaining his Outperform rating yet drops his stock forecast from $427 to $414.

Rockwell Automation

Reported its first quarter results for 2023, which reflect an increase of 6.7% year over year in sales and an organic growth rate of 9.9%. Currency translation reduced sales by 4.0%, while acquisitions contributed 0.8%. Organic total earnings before interest and tax (EBRIE) were up 14%, while diluted earnings per share (EPS) and adjusted earnings per share (adjusted EPS) rose 61% and 15% respectively year over year.

Rockwell also updated their fiscal 2023 guidance, including a projected reported sales growth rate between 10.0% and 14.0%, as well as between 11.0% and 15.0% for organic sales growth from the same period last year. They anticipate adjusted diluted EPS to be in the range of $10.99 to $11.79, with overall adjusted EPS estimated at $10.70 – $11 ‘.50 for the same period of In total revenue from the Fiscal 2023’s first quarter was recorded at $1,981 million, a significant 6 .7 % increase compared to the first quarter of fiscal 2022’s revenue of $1,857 million.

- Citigroup analyst Andrew Kaplowitz maintains a Buy rating for Rockwell Automation and is increasing the price target from $297 to $320.

- Oppenheimer analyst Noah Kaye has an Outperform rating is and elevating the target price from $290 to $294.

- Goldman Sachs analyst Joe Ritchie held a Sell however he raised the target price from $238 to $272.

- Barclays analyst Julian Mitchell maintained an Equal Weight with a rise in his price target from $220 up to $250.

- Baird analyst Richard Eastman increased his stock forecast to $292 while staying with an Outperform rating.

- Mizuho analyst Brett Linzey reiterated her Neutral designation alongside raising to $260 price target, up from $250.

Mobileye

Reported 27 cents of adjusted earnings per share for $565 million in sales. This exceeded Wall Street expectation of 17 cents of a share on sales of $533 million. For 2023, Mobileye forecasts sales to hover between $2.2 billion and $2.3 billion with an expected operating profit that could range from $580 million up to $630 million. Currently, analysts project revenue coming in just below the estimated range at roughly $2.2 billion but still predicted an extended rate of growth into 2025 with higher expectations at around $4 billion by then.

- Mizuho’s Vijay Rakesh upped his price target from $40 to $42 while maintaining a Buy rating.

- Needham’s Rajvindra Gill’s increase his price target from $43 to $45 while also keeping a Buy rating unchanged.

- Cowen & Co.’s Joshua Buchalter opted for an Outperform rating with increasing his price target from $35 up to $42.