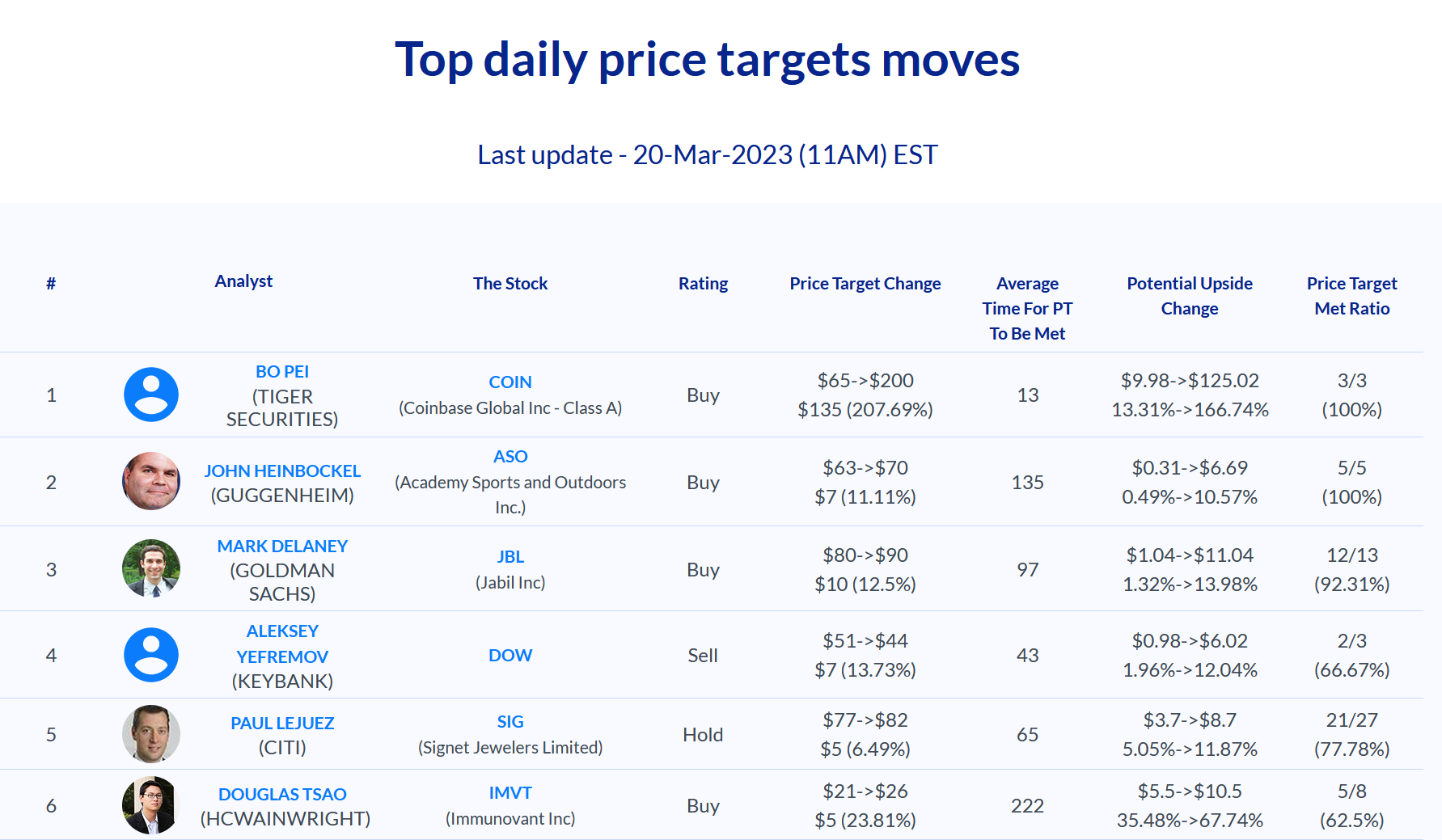

Daily Update - March 20, 2023

Selected highlights of the day

By: Matthew Otto

UBS Group’s takeover of Credit Suisse Group

Is reportedly imminent, with the two banks expected to announce the merger soon. The Swiss government is said to be providing 9 billion Swiss francs to backstop potential losses that UBS may take on in the deal. Under the terms of the merger agreement, all shareholders of Credit Suisse will receive one share in UBS for 22.48 shares in Credit Suisse, putting the deal’s price at around 3 billion Swiss francs ($3.2 billion).

Over the weekend credit rating agency S&P Global Ratings downgraded First Republic Bank’s credit rating from A- to BBB+. The downgrade is due to concerns over the bank’s asset quality, which S&P Global Ratings believes has weakened in recent quarters. The rating agency also noted that the bank’s credit losses are likely to rise in the coming quarters, driven by the pandemic and the potential for future economic volatility.

GENI

It seems like there are different opinions among analysts regarding Genius Sports’ potential.

- JMP Securities and BTIG analysts are bullish on the stock, with Jordan Bender and Clark Lampen issuing Market Outperform and Buy ratings, respectively, and setting price targets of $7 and $6.

- Needham analyst Bernie McTernan maintains a Buy rating and a price target of $7.

Pear Therapeutics

Has withdrawn its revenue and operating guidance for fiscal years 2022 and 2023.

- Credit Suisse analyst Judah Frommer has downgraded the company’s rating from Outperform to Neutral and lowered the price target from $7 to $1.

- TD Cowen analyst Charles Rhyee has also downgraded Pear Therapeutics’ rating from Outperform to Market Perform.

- Chardan Capital analyst Keay Nakae has downgraded the company’s rating from Buy to Neutral but announced a higher price target of $8.

DELL

Goldman Sachs analyst Michael Ng has initiated coverage on Dell Technologies with a Buy rating. NG believes that while the demand for personal computers has surged due to the pandemic, the challenges associated with supply chain disruptions and component shortages will eventually subside, resulting in a more normalized PC market. In addition, the analyst believes that Dell’s strong market position in the PC market and its expanding enterprise solutions offerings position the company for future growth.

ENPH

Enphase Energy has expanded its IQ8 microinverter deployments in Virginia, with installers reporting growing deployments of Enphase Energy Systems powered by IQ8 microinverters. According to industry reports, residential solar deployments in Virginia are expected to reach around 104 MW in 2023, representing a 37% increase from 2021. Enphase’s IQ8 micro inverters are designed to maximize the value for homeowners who want battery backup by eliminating sizing restrictions when paired with IQ batteries. The IQ8 microinverters also come with a 25-year limited warranty.

- Raymond James analyst Pavel Molchanov has upgraded Enphase Energy from Market Perform to Outperform and announced a $225 price target.

AMZN

- Needham analyst Laura Martin has reiterated her Buy rating on Amazon.com and maintained a $120 price target.

PTON

- John Blackledge upgraded Peloton from Market Perform to Outperform and raised the price target to $80, citing the company’s improving supply chain, growth potential in international markets, and strong demand for its connected fitness products

PLBY Group

Owner of Playboy, has reported its financial results for the fourth quarter and full year ended December 31, 2022. The company’s revenue grew 8% year-over-year to $266.9 million in fiscal year 2022, while the net loss was $277.7 million and adjusted EBITDA loss was $6.6 million. The company’s CEO, Ben Kohn, has announced that the company is undergoing a strategic review to restructure and simplify its business, moving to a capital-light model entirely focused on its most valuable brands, Playboy and Honey Birdette. The restructuring is expected to eliminate a minimum of $15 million of costs on an annualized basis and reduce operational complexity by eliminating unprofitable business units and non-core assets. It’s important to note that investing in newly restructured companies can be risky, and investors should always conduct their own research and analysis before making investment decisions.

- It appears that Chardan Capital analyst Brian Dobson has reiterated his Buy rating on PLBY Group and maintained a $5 price target.

AQN

Last Friday, on March 17, 2023, Algonquin Power & Utilities announced its financial results for the fourth quarter and year ended December 31, 2022. The company reported fourth quarter adjusted EBITDA of $358.3 million, an increase of 20%, and adjusted net earnings of $151.0 million, an increase of 10%. The company’s annual adjusted EBITDA was $1,256.8 million, an increase of 17%, and annual adjusted net earnings were $474.9 million, an increase of 6%. However, annual adjusted net earnings per common share decreased by 3% year-over-year. The company also announced a pending acquisition of Kentucky Power Company and AEP Kentucky Transmission Company, Inc. and the completion of its inaugural asset recycling transaction. In addition, the company announced decisive actions to support its long-term energy transition strategy, including a reset of its quarterly dividend, reduced capital intensity, and the intention to raise approximately $1 billion in asset sales.

In its outlook, Algonquin Power & Utilities Corp. has reiterated its previously-disclosed estimate of adjusted net earnings per common share for the 2023 fiscal year within a range of $0.55-$0.61. The company’s estimate for 2023 adjusted net earnings per common share is based on certain assumptions and should be read in conjunction with the Annual MD&A. The company also expects to spend approximately $3.6 billion on capital investment opportunities in the 2023 fiscal year, assuming the closing of the $2.646 billion Kentucky Power Transaction, with most of the investment expected to be made by the Regulated Services Group.

- Wells Fargo analyst Neil Kalton has maintained his “Overweight” rating on Algonquin and raised the price target from $9 to $9.5.

- RBC Capital analyst Nelson Ng has reiterated a “Sector Perform” rating and maintained a price target of $8.The stock has lost 50% since its peak of April last year.

Aveanna Healthcare

Announced last Thursday its financial results for Q4 2022 and the full year 2022. The company’s Q4 2022 revenue increased 9.0% to $451.1 million compared to the same period in 2021. The gross margin increased 3.5% to $128.8 million. However, the net loss was $237.8 million, and adjusted EBITDA decreased 35% to $29.7 million. For the full year 2022, revenue increased 6.5% to $1,787.6 million. The gross margin was $553.2 million, and adjusted EBITDA was $129.3 million. The net loss for the year was $662.0 million. The company reported having cash of $19.2 million and borrowing capacity of $35.0 million under its securitization facility as of December 31, 2022. Additionally, Aveanna Healthcare Holdings provided its full year 2023 guidance with revenue expected to be at least $1,840 million and adjusted EBITDA of at least $130 million.

- Following the news a day after Truist Securities’ analyst David Macdonald keeps his Hold rating on Aveanna Healthcare Holdings and increases the price target from $1 to $1.4.

- Today, Raymond James analyst John Ransom maintains his Strong Buy rating on Aveanna Healthcare Holdings yet he lowers his price target from $4 to $3, while RBC Capital analyst Ben Hendrix maintains his Sector Perform rating on the company and lowers the price target from $3 to $2.