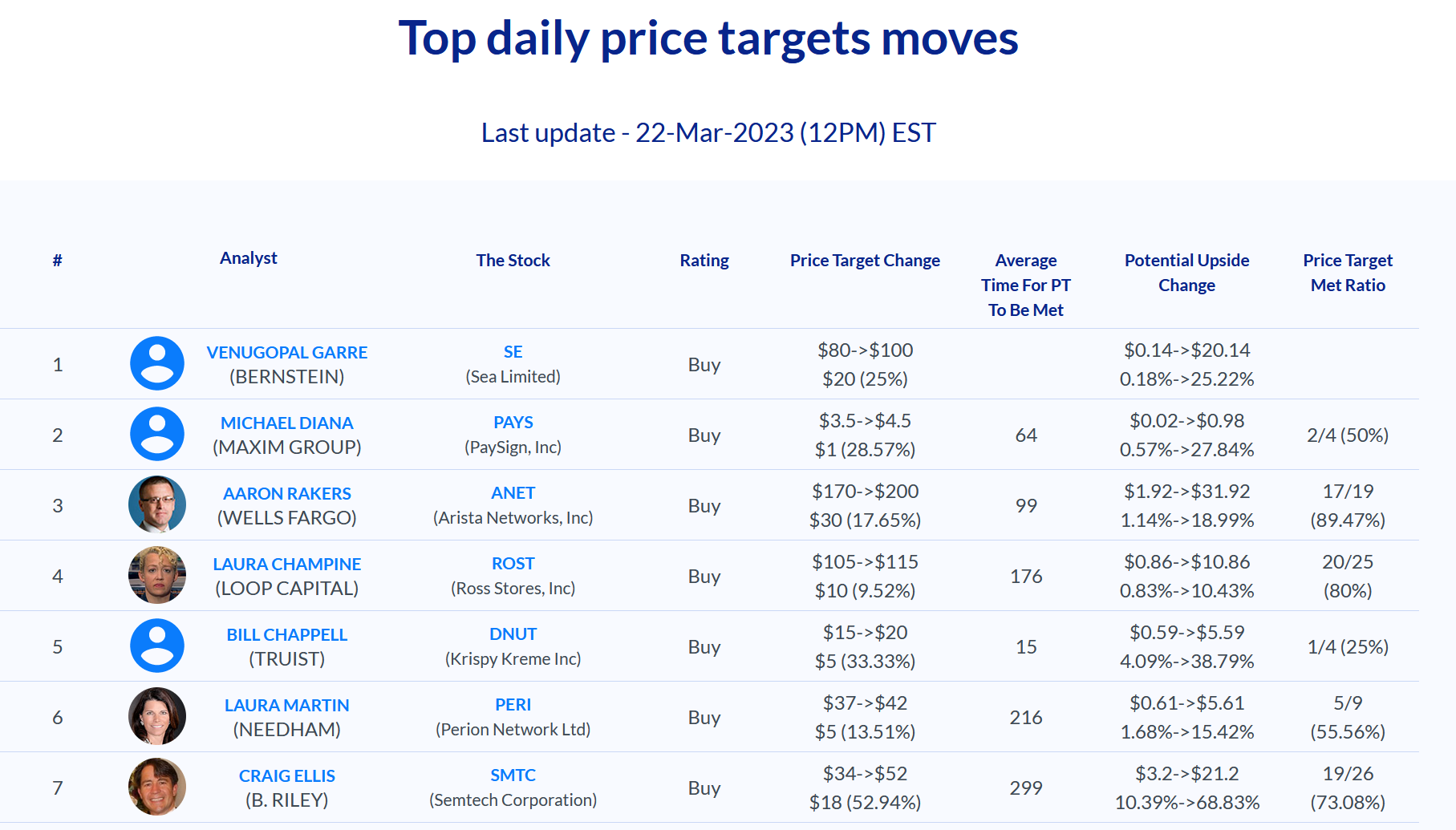

Daily Update - March 22, 2023

Selected highlights of the day

By: Matthew Otto

NKE

Nike’s fiscal third-quarter earnings and revenue exceeded Wall Street expectations, though the company continues to face challenges such as excess inventory and soft sales in China. The sportswear retailer’s gross margin for the quarter fell to 43.3% due to higher markdowns and promotions that Nike used to liquidate its inventory. Inventories were up 16% from the previous year, with $8.9 billion worth of inventory. The company is taking a cautious approach to planning given concerns about consumer confidence and the economy. Nike CEO John Donahoe is confident about the company’s momentum in China despite sales falling 8% to $1.99 billion during the quarter. In contrast, double-digit sales increases were seen in all other markets, with North America up 27% and Europe, Middle East and Africa up 17%. Nike’s direct-to-consumer sales were up 17% during the holiday quarter, with Nike digital sales jumping 20%.

Nike beat Wall Street’s estimates for its Q3 earnings and revenue. Analysts had expected earnings per share of 55 cents, but Nike reported earnings per share of 79 cents. Similarly, analysts had forecasted revenue of $11.47 billion, but Nike reported revenue of $12.39 billion

- Guggenheim analyst Robert Drbul boosted the price target from $135 to $145 while sustaining a Buy rating.

- Jefferies analyst Randal Konik raised the price target from $140 to $160 while keeping a Buy rating.

- Piper Sandler analyst Abbie Zvejnieks hiked up the price target from $145 to $220 while maintaining a Neutral rating.

- RBC Capital analyst Piral Dadhania set the price target at $145 while reaffirming an Outperform rating.

- Wedbush analyst Tom Nikic maintained an Outperform rating but

- Stifel analyst Jim Duffy increased the price target from $132 to $143 while retaining a Buy rating.

- TD Cowen analyst John Kernan raised the price target from $141 to $142 while sustaining an Outperform rating.

- Goldman Sachs analyst Kate McShane upped her price target from $134 to $148 while maintaining a Buy rating.

- JP Morgan analyst Matthew Korn decreased the price target from $156 to $152 while keeping an Overweight rating.

- Raymond James analyst Rick Patel bumped up the price target from $130 to $135 while maintaining an Outperform rating.

- Wells Fargo analyst Kate Fitzsimons lowered her price target from $146 to $142 while keeping an Equal-Weight rating.

- Citigroup analyst Paul Lejuez increased the price target from $115 to $125 while sustaining a Neutral rating.

- Credit Suisse analyst Michael Binetti raised the price target from $132 to $139 while keeping an Outperform rating.

- Baird analyst Jonathan Komp lifted his price target from $130 to $138 while sustaining an Outperform rating.

- Barclays analyst Adrienne Tennant increased her price target from $110 to $154 while upgrading from Equal-Weight to Overweight.

- UBS analyst Jay Sole raised the price target from $151 to $155 while maintaining a Buy rating.

- Telsey Advisory Group analyst Joseph Feldman increased the price target from $138 to $140 while sustaining an Outperform rating.

NVDA

Nvidia announced new AI products and partnerships at its GPU Technology Conference this week, including the DGX cloud service and co-development of AI models with Adobe and other companies. Wall Street analysts were enthusiastic about the news, with Needham’s Rajvindra Gill rating the stock as Buy and predicting strong demand for the coming DGX H100 AI computer systems. Nvidia’s all-in-one solution for AI-related tasks, including chips, databases, and computing capacity, has helped it segment itself in a crowded field.

- BMO Capital analyst Ambrish Srivastava raised the price target from $255 to $305 while maintaining an Outperform rating.

- TD Cowen analyst Matthew Ramsay increased the price target from $260 to $300 while maintaining an Outperform rating.

- Rosenblatt analyst Hans Mosesmann reiterated a Buy rating and raised the price target by 80% from the previous target.

- Mizuho analyst Vijay Rakesh increased the price target from $230 to $290 while maintaining a Buy rating.

- Wells Fargo analyst Aaron Rakers increased the price target by 83% from $275 to $320 while maintaining an Overweight rating.

- Oppenheimer analyst Patrick Scholes increased the price target from $275 to $300 while maintaining an Outperform rating.

- Needham analyst Rajvindra Gill reiterated a Buy rating.

- Deutsche Bank analyst Ross Seymore maintained a Hold rating and raised the price target from $200 to $220.

SPOT

- Guggenheim analyst Michael Morris lifted Spotify Technology from Neutral to Buy and raised his price target from $120 to $155.

Morris was bullish on Spotify in 2022 when it dropped from $234 to $80 in 2022.

COIN

On Tuesday, the US Supreme Court heard arguments in a case brought by Coinbase Global. The cryptocurrency exchange is appealing against lower court decisions allowing proposed class action lawsuits to proceed. Coinbase is seeking to have the claims moved out of courts and into private arbitration. The company argues that its user agreement requires disputes to be resolved through arbitration and that, under the Federal Arbitration Act, which governs dispute resolution proceedings through arbitration, action in trial courts must stop when a request to compel arbitration is denied. Some justices expressed doubt over Coinbase’s arguments, while others raised concerns about the consequences for defendants seeking to arbitrate customer claims. A ruling is expected by the end of June.

- Barclays analyst Benjamin Budish had Coinbase with an Equal-Weight and his stock forecast upgraded from $63 to $86.

Onon

Continues with the coverage following its positive earnings news from Monday.

- Baird analyst Jonathan Komp raised the price target from $31 to $33 while maintaining an Outperform rating.

- Credit Suisse analyst Michael Lapides boosted the price target from $28 to $33 while maintaining an Outperform rating.

- Morgan Stanley analyst Alex Straton lifted the price target from $26 to $33 while maintaining an Overweight rating.

- Telsey Advisory analyst Joseph Feldman raised the price target from $30 to $33 while maintaining an Outperform rating.

Knight-Swift Transportation

Has reached an agreement to acquire U.S. Xpress Enterprises, Inc. for a total enterprise value of approximately $808 million, excluding transaction costs. The deal has been unanimously approved by the Board of Directors of Knight-Swift and a Special Committee of the independent directors of the U.S. Xpress Board of Directors. The transaction is expected to close late in the second quarter or early third quarter of 2023, subject to customary closing conditions. After the deal is completed, U.S. Xpress will continue as a separate brand and operation, with the Fullers and Eric Peterson, CFO, transitioning out of their executive officer roles. Knight-Swift aims to grow its revenue base by nearly 30% and reach mid-teens return on invested capital for U.S. Xpress by calendar 2026.

- Wolfe Research analyst Scott Group has his price target at $65 and upgraded the rating from Peer Perform to Outperform.

- TD Cowen analyst Jason Seidl increased his price target from $67 to $70 and maintained the rating as Outperform.

- Stifel analyst Bert Subin lowered his price target from $71 to $66 but maintained the rating as a Buy.