Selected stock price target news of the day - December 6th, 2024

By: Matthew Otto

Five Below Surpasses Q3 Earnings and Revenue Expectations, Raises Full-Year Guidance

Five Below delivered its Q3 2024 results, with adjusted EPS of $0.42, surpassing analyst estimates of $0.17 by $0.25. Revenue for the quarter reached $843.7 million, exceeding the consensus estimate of $796 million and marking a 14.6% increase from $736.4 million in Q3 2023.

Comparable sales rose by 0.6%. Five Below’s adjusted operating income totaled $27.6 million, while GAAP net income was $1.7 million. Store expansion remained with 82 new locations opened during the quarter, raising the total store count to 1,749 across 44 states, representing an 18.1% year-over-year increase.

For fiscal year 2024, Five Below increased its guidance, projecting adjusted EPS of $4.78 to $4.96, exceeding the consensus estimate of $4.61. Five Below anticipates revenue of $3.84 to $3.87 billion, compared to the consensus forecast of $3.8 billion.

Year-to-date performance highlighted an 11.9% increase in net sales to $2.49 billion, despite a 2.6% decline in comparable sales. Adjusted net income for the year-to-date period was $85.5 million, with adjusted diluted EPS of $1.55.

Analysts Raise Targets as Q3 Beats Estimates and Updates Guidance

- Mizuho analyst David Bellinger kept a Neutral rating but increased the price target from $90 to $105.

- Loop Capital analyst Anthony Chukumba reiterated a Hold rating while raising the price target from $90 to $120.

- JP Morgan analyst Matthew Boss maintained an Underweight rating yet boosted the price target from $83 to $110.

- Craig-Hallum analyst Jeremy Hamblin upheld a Buy rating and elevated the price target from $125 to $150.

- Truist Securities analyst Scot Ciccarelli continued with a Hold rating and raised the price target from $88 to $118.

- Barclays analyst Karen Short kept with an Equal-Weight rating but lifted the price target from $90 to $100.

- Wells Fargo analyst Edward Kelly reaffirmed an Overweight rating and enhanced the price target from $115 to $135.

- Guggenheim analyst John Heinbockel maintained a Buy rating and raised the price target from $125 to $140.

- Morgan Stanley analyst Simeon Gutman held an Equal-Weight rating while increasing the price target from $100 to $120.

- Telsey Advisory Group analyst Joseph Feldman reiterated a Market Perform rating and adjusted the price target from $95 to $115.

Which Analyst has the best track record to show on FIVE?

Analyst Judah Frommer (CREDIT SUISSE) currently has the highest performing score on FIVE with 10/10 (100%) price target fulfillment ratio. His price targets carry an average of $23.5 (30.72%) potential upside. Five Below stock price reaches these price targets on average within 73 days.

Campbell’s Q1 FY 2025 Results Show Mixed Performance and Leadership Change Amid Market Challenges

Campbell Soup Company reported first-quarter fiscal 2025 results, with adjusted earnings per share (EPS) of $0.89, exceeding analyst estimates by $0.01. Revenue reached $2.8 billion, aligning with consensus expectations, reflecting a 10% year-over-year increase driven by the Sovos Brands acquisition.

However, organic net sales decreased 1%, impacted by flat volume/mix and a 1% decline in net price realization. Adjusted EBIT grew 6% to $432 million, supported by Sovos’ contributions, while adjusted gross profit margins fell 70 basis points to 31.4% due to inflation and acquisition-related costs. Cash flow from operations rose to $225 million, up from $174 million, benefiting from favorable working capital changes.

Looking ahead, Campbell reaffirmed its fiscal 2025 guidance, projecting EPS of $3.12 to $3.22, in line with the consensus of $3.17, and net sales growth of 9% to 11%. Campbell faces headwinds, including weak consumer spending and declining snack segment sales, which fell 2% organically year-over-year.

Analysts offered mixed perspectives: D.A. Davidson analyst Brian Holland maintained a Neutral rating with a $51 price target, highlighting Sovos’ strong performance. On the other hand, Bank of America analyst Bryan Spillane reiterated an Underperform rating and a $46 target, citing tougher growth prospects compared to industry peers.

Analysts Adjust Targets Amid Mixed Earnings

- Stifel analyst Matthew Smith maintained a Hold rating and lowered the price target from $50 to $47.

- Citigroup analyst Thomas Palmer reiterated a Sell rating and cut the price target from $44 to $41.

- RBC Capital analyst Nik Modi maintained a Sector Perform rating and the price target at $51.

- Wells Fargo analyst Chris Carey upheld an Equal-Weight rating but reduced the price target from $51 to $45.

- DA Davidson analyst Brian Holland reiterated a Neutral rating with a $51 price target.

- Stephens & Co. analyst Jim Salera reaffirmed an Overweight rating.

Which Analyst has the best track record to show on CPB?

Analyst Robert Moskow (TD COWEN) currently has the highest performing score on CPB with 23/24 (95.83%) price target fulfillment ratio. His price targets carry an average of $1.22 (2.45%) potential upside. Campbell Soup Company stock price reaches these price targets on average within 354 days.

nCino Misses Q4 Revenue Guidance Expectations, Despite Strong Q3 Results and EPS Performance

nCino reported its financial results for the third quarter of fiscal 2025, with total revenues reaching $138.8 million, a 14% increase from $121.9 million in the same period of the previous year. Revenue surpassed analyst expectations, with the consensus estimate at $137.34 million.

Subscription revenues also grew by 14%, totaling $119.9 million, up from $104.8 million in Q3 FY24. GAAP operating margin improved to -1%, up approximately 1,000 basis points year-over-year, while non-GAAP operating margin stood at 20%, reflecting a 350 basis point increase.

nCino reported Q3 EPS of $0.21, beating analyst expectations by $0.05, with the consensus estimate at $0.16. GAAP net loss for the quarter was $5.3 million, narrowing from a loss of $16.4 million a year ago, while non-GAAP net income attributable to nCino grew by 51% to $24.4 million, compared to $16.2 million in Q3 FY24.

Remaining performance obligation (RPO) reached $1.095 billion, an increase of 19% compared to $917.1 million at the same time last year, with $730 million expected to be recognized over the next 24 months. nCino’s cash position stood at $258.3 million.

Looking ahead, nCino is providing guidance for fiscal year 2025, projecting EPS of $0.75 to $0.76, above the consensus estimate of $0.62. Total revenues are expected to be between $539 million and $541 million, compared to the consensus of $541.6 million.

For Q4 FY2025, nCino expects EPS of $0.18 to $0.19, surpassing the consensus estimate of $0.17, with revenues between $139.5 million and $141.5 million, below the consensus of $143.8 million.

Analyst Ratings Mixed Following Q3 FY2025 Results

- Morgan Stanley analyst James Faucette maintained an Equal-Weight rating but lowered the price target from $41 to $39.

- Keefe, Bruyette & Woods analyst Ryan Tomasello kept an Outperform rating, yet lowered the price target from $49 to $44.

- Baird analyst Joe Vruwink maintained a Neutral rating while reducing the price target from $43 to $42.

- Stephens & Co. analyst Charles Nabhan held an Equal-Weight rating, but raised the price target from $35 to $38.

- Needham analyst Mayank Tandon kept a Buy rating and increased the price target from $40 to $45.

- Piper Sandler analyst Brent Bracelin downgraded from Overweight to Neutral, maintaining the price target at $38.

Which Analyst has the best track record to show on NCNO?

Analyst Charles Nabhan (STEPHENS) currently has the highest performing score on NCNO with 9/9 (100%) price target fulfillment ratio. His price targets carry an average of $5.26 (17.69%) potential upside. nCino stock price reaches these price targets on average within 69 days.

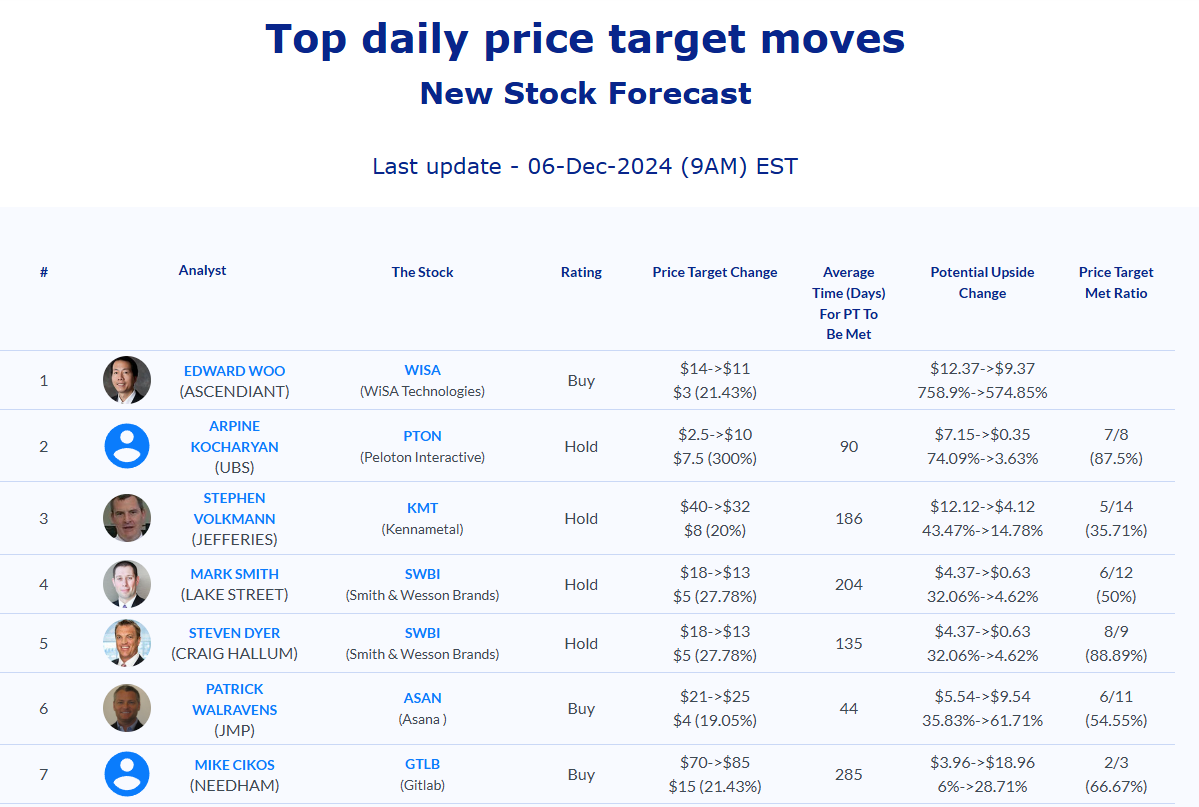

Daily stock Analysts Top Price Moves Snapshot