Selected stock price target news of the day - June 27th, 2024

By: Matthew Otto

BlackBerry Misses Earnings Estimates in Q1 FY2025 Despite Revenue Beat, Issues Mixed FY2025 Guidance

BlackBerry reported first quarter for fiscal year 2025 with a Q1 EPS of ($0.07), which was $0.02 worse than the analyst estimate of ($0.05). Achieved a total revenue of $144 million, surpassing the consensus estimate of $132.05 million. Revenue contributions were $53 million from IoT, $85 million from cybersecurity, and $6 million from licensing and other sources.

The IoT division’s revenue was driven by royalties, particularly in the automotive sector, which accounted for 80% of the division’s total revenue. Gross margin for the IoT division stood at 81%, bolstered by professional services and royalties.

In the cybersecurity division, BlackBerry saw improvements such as annual recurring revenue increased to $285 million, and the dollar-based net retention rate rose to 87%. The division’s revenue achieved $85 million driven by the SecuSmart business and improved ARR.

BlackBerry reiterated its full-year outlook, expecting FY2025 EPS of ($0.03) to ($0.07) compared to the consensus of ($0.04) and revenue between $586 million and $616 million versus the consensus of $601 million. For Q2 2025, BlackBerry projects EPS of ($0.02) to ($0.04) against the consensus of ($0.02) and revenue between $136 million and $144 million, versus the consensus of $142 million.

Analyst Reactions: Mixed Ratings and Target Adjustments

- Canaccord Genuity analyst Kingsley Crane maintained a Hold rating and lowered the price target from $3.25 to $2.7.

- CIBC analyst Todd Coupland upgraded from Neutral to Outperformer.

- Baird analyst Luke Junk maintained a Neutral rating and lowered the price target from $3.5 to $3.

Which Analyst has the best track record to show on BB?

Analyst Paul Treiber (RBC) currently has the highest performing score on BB with 14/16 (87.5%) price target fulfillment ratio. His price targets carry an average of $0.12 (4.17%) potential upside. BlackBerry stock price reaches these price targets on average within 66 days.

Micron Technology Exceeds Q3 Expectations, Offers Cautious Outlook for Q4 Amid AI Demand

Micron Technology announced its financial results for the fiscal third quarter of 2024, reporting revenues of $6.81 billion and adjusted earnings per share of 62 cents. Both revenue and earnings per share surpassed the consensus estimates of $6.67 billion and 51 cents, respectively. Reported a net income of $332 million, or 30 cents per share, an improvement from the net loss of $1.9 billion, or $1.73 per share, in the same quarter last year.

For the fiscal fourth quarter of 2024, Micron projects an EPS in the range of $1 to $1.16, slightly below the consensus estimate of $1.02. Revenue guidance for the same period is expected to range between $7.4 billion and $7.8 billion, which falls short of the consensus estimate of $7.59 billion.

Analysts Bullish with Raised Price Targets Following Q3 Results

- Goldman Sachs analyst Toshiya Hari maintained a Buy rating and raised the price target from $138 to $158.

- Wedbush analyst Matt Bryson reiterated an Outperform rating and a $170 price target.

- KeyBanc analyst John Vinh maintained an Overweight rating and increased the price target from $150 to $160.

- Piper Sandler analyst Harsh Kumar kept an Overweight rating and upgraded the price target from $130 to $150.

- Needham analyst Quinn Bolton maintained a Buy rating and raised the price target from $120 to $150.

Which Analyst has the best track record to show on MU?

Analyst Brian Chin (STIFEL) currently has the highest performing score on MU with 6/8 (75%) price target fulfillment ratio. His price targets carry an average of $21.02 (21.24%) potential upside. Micron Technology stock price reaches these price targets on average within 24 days.

Progress Software Exceeds Expectations in Q2 2024 Results and Issues Positive Guidance

Progress Software has announced its financial results for the second quarter of fiscal 2024, reporting earnings per share of $1.08, outperforming the analyst consensus estimate of $0.95 by $0.13. Revenue for the quarter reached $175 million, exceeding the consensus estimate of $168.42 million. Annual Recurring Revenue grew by 1% to $579 million. Additionally, Progress maintained its balance sheet with $190 million in cash and equivalents, and a debt position of $810 million, contributing to a net debt of $620 million.

Looking ahead, Progress Software provided guidance for the third quarter of 2024, expecting EPS in the range of $1.11 to $1.15, compared to the consensus estimate of $1.21. Revenue for Q3 is projected to be between $174 million and $178 million, slightly below the consensus estimate of $183.52 million.

For the full fiscal year 2024, Progress Software anticipates EPS between $4.70 and $4.80, surpassing the consensus estimate of $4.69. Full-year revenue guidance is set between $725 million and $735 million, which exceeds the consensus estimate of $726.5 million.

Analysts Maintain Mixed Ratings and Targets Following Q2 Results

- DA Davidson analyst Lucky Schreiner maintained a Buy rating with a $65 price target.

- Oppenheimer analyst Ittai Kidron reiterated an Outperform rating with a $66 price target.

- Jefferies analyst Brent Thill kept a Hold rating but lowered the price target from $60 to $55.

- Guggenheim analyst Raymond McDonough reiterated a Buy rating with a $64 price target.

Which Analyst has the best track record to show on PRGS?

Analyst Ittai Kidron (OPPENHEIMER) currently has the highest performing score on PRGS with 3/7 (42.86%) price target fulfillment ratio. His price targets carry an average of $13.37 (25.40%) potential upside. Progress Software stock price reaches these price targets on average within 450 days.

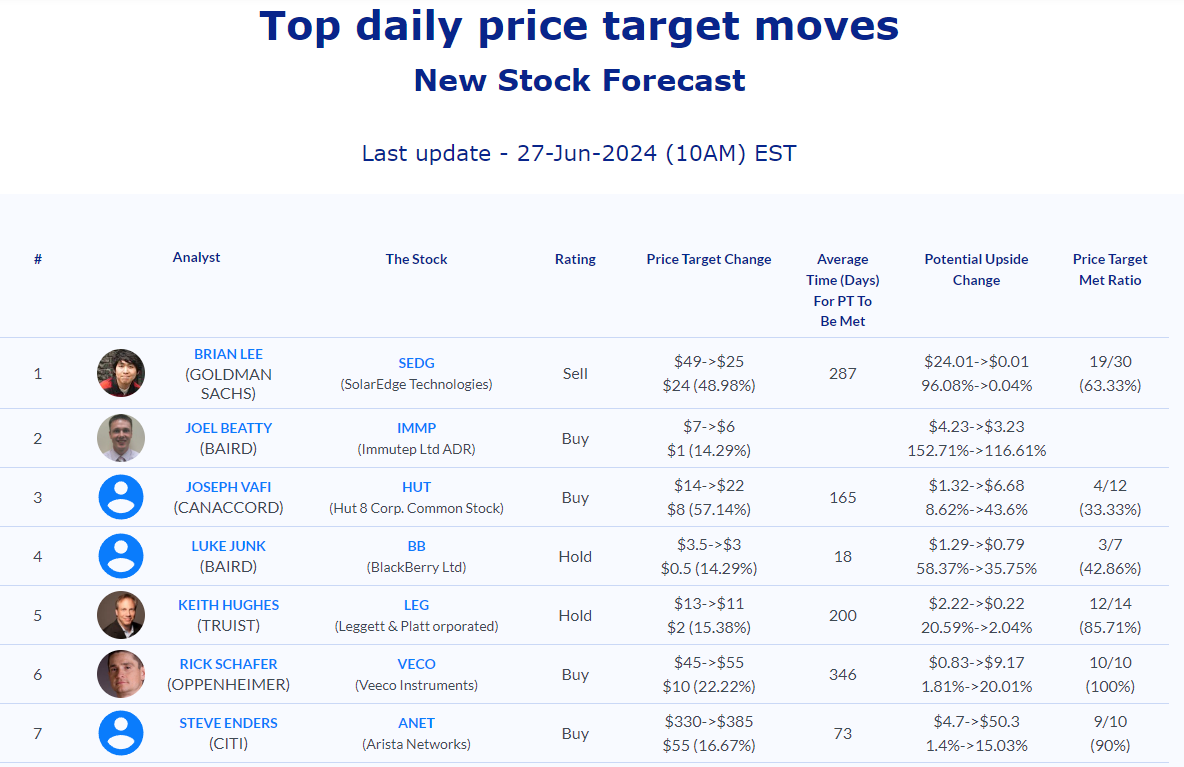

Daily stock Analysts Top Price Moves Snapshot