Selected stock price target news of the day - June 27th, 2025

By: Matthew Otto

Nike Q4 Results Exceed EPS Forecasts Amid Broad-Based Revenue Decline

Nike reported fiscal 2025 fourth-quarter revenue of $11.1 billion, a 12% year-over-year decline, but above the consensus estimate of $10.7 billion compiled by LSEG. Diluted earnings per share (EPS) for the quarter came in at $0.14, $0.02 higher than analyst expectations of $0.12.

Full-year revenue was $46.3 billion, down 10% on a reported basis and 9% on a currency-neutral basis. Gross margin in Q4 fell by 440 basis points to 40.3%, driven by higher discounts and a shift in channel mix. Direct-to-consumer revenue for the quarter was $4.4 billion, down 14%, largely due to a 26% decline in digital sales, while Nike-owned retail stores saw a 2% increase.

Wholesale revenue declined 9% to $6.4 billion, and Converse revenue dropped 26% to $357 million. Net income for the quarter was $200 million, down 86% from the same period last year. For the full fiscal year, net income fell 44% to $3.2 billion, while EPS decreased 42% to $2.16.

Citi analyst Monique Pollard highlighted that Nike’s renewed focus on running—supported by new iterations of the Pegasus and Vomero—contributed to a category rebound in Q4, following several quarters of weakness. Nike increased marketing spend by 15% year-over-year to $1.3 billion, reflecting higher sports marketing and brand campaign investments. CFO Matthew Friend stated on the earnings call that the company is actively working to offset macroeconomic and geopolitical pressures, including U.S. tariffs that could add an estimated $1 billion to costs.

Analysts Adjust Price Targets Following Q4 Results and Updates

- Telsey Advisory Group analyst Cristina Fernandez maintained a Market Perform rating and the price target at $70.

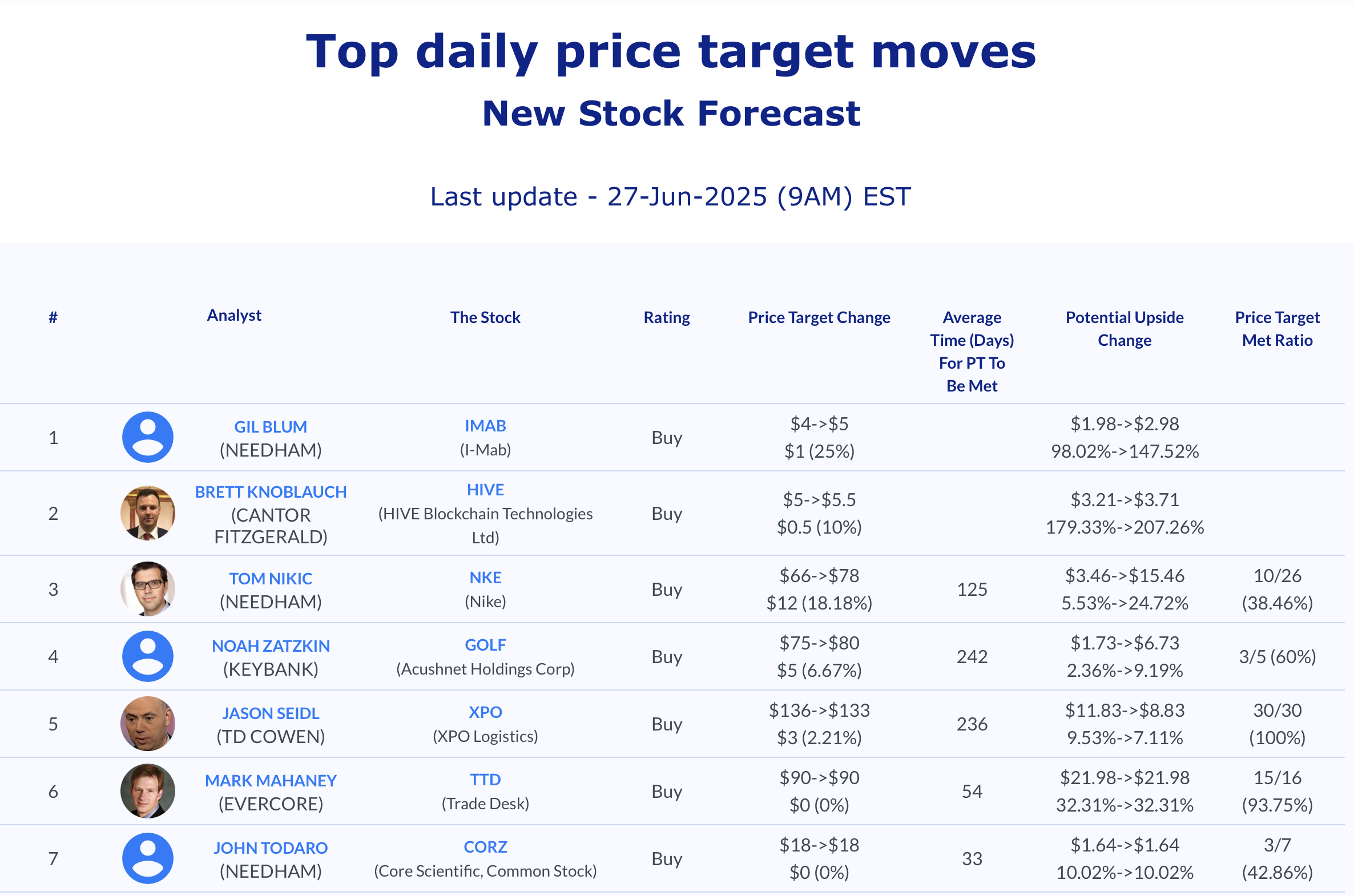

- Needham analyst Tom Nikic reiterated a Buy rating and raised the price target from $66 to $78.

- Morgan Stanley analyst Alex Straton increased the price target to $64.

- Evercore ISI analyst Michael Binetti held a Buy rating and lifted the price target from $75 to $90.

- Citi analyst Paul Lejuez maintained a Neutral rating and raised the price target from $57 to $68.

- Truist Securities analyst Joseph Civello increased the price target to $85.

- Williams Trading analyst Sam Poser reiterated a Buy rating and a $73 price target.

- JPMorgan analyst Matthew Boss increased the price target to $64.

Which Analyst has the best track record to show on NKE?

Analyst Paul Lejuez (CITI) currently has the highest performing score on NKE with 19/25 (76%) price target fulfillment ratio. His price targets carry an average of $-0.31 (-0.54%) potential downside. Nike stock price reaches these price targets on average within 141 days.

First Financial to Acquire Westfield; Capital and Earnings Outlook Stable

First Financial Bancorp announced a definitive agreement to acquire Westfield Bancorp in a cash-and-stock transaction valued at approximately $325 million. According to KBRA, which rates First Financial’s senior unsecured debt at BBB+ with a Stable Outlook, the deal represents a price of 1.4x tangible book value at announcement and includes 80% cash and 20% stock consideration.

Westfield holds $2.2 billion in assets, which will account for roughly 11% of the combined company’s pro forma total assets. Upon closing—expected in Q4 2025 pending regulatory approvals—First Financial will grow to $20.6 billion in total assets and become the 8th largest bank by deposit market share in Ohio, ranking 4th among locally headquartered banks. No changes are anticipated to FFBC’s management or Board, although some Westfield executives are expected to take leadership roles in the combined institution.

The transaction is expected to moderately reduce First Financial’s capital ratios, with pro forma tangible common equity (TCE) and common equity tier 1 (CET1) ratios projected at 7.4% and 10.9%, respectively. Management plans to rebuild capital toward a TCE target range of 7.5%–8% through internal earnings, citing 60 basis points of CET1 expansion over the past year.

First Financial’s commercial lending focus will remain intact, and the loan-to-deposit ratio is projected at 82%, supporting continued loan growth. Cost synergies are expected to reach 75% of a modeled 40% of Westfield’s standalone expenses, driving management’s projected 2026 return on assets (ROA) of 1.4%. Although revenue diversification may decline slightly—Westfield reported 16% noninterest income versus FFBC’s 29% in Q1 2025—management anticipates potential cross-selling opportunities in fee-based services.

Credit quality remains, supported by a 1.1% loan mark and an NCO ratio averaging 5 bps since 2013. A 50% review of Westfield’s commercial portfolio was completed during due diligence, and the risk of negative surprises appears limited.

Analyst Reiterates Rating Following Acquisition Announcement

- Stephens & Co. analyst Terry McEvoy reiterated with an Overweight rating and a $29 price target.

Which Analyst has the best track record to show on FFBC?

Analyst Terry Mcevoy (STEPHENS) currently has the highest performing score on FFBC with 4/6 (66.67%) price target fulfillment ratio. His price targets carry an average of $5.27 (19.00%) potential upside. First Financial Bancorp stock price reaches these price targets on average within 732 days.

Orion Energy Systems Reports FY’25 Results; Projects Growth in FY’26

Orion Energy Systems reported fiscal fourth quarter (Q4’25) earnings per share (EPS) of ($0.09), falling short of the analyst consensus estimate of ($0.05) by $0.04. Quarterly revenue totaled $20.9 million, below the consensus estimate of $24.77 million, and declined 21% from $26.4 million in Q4’24.

The drop was mainly attributed to a 33% year-over-year decline in LED lighting revenue and a 21% decrease in maintenance revenue. These were partially offset by an 18% increase in EV charging revenue, which reached $5.8 million in Q4. Gross margin for the quarter improved to 27.5%, up from 25.8% in the prior-year period. Orion achieved positive adjusted EBITDA and ended the year with $6 million in cash and $13 million in total liquidity.

For fiscal year 2025 (FY’25), total revenue declined 12% to $79.7 million, with LED lighting and maintenance segments down 22% and 11%, respectively. EV charging revenue rose 37% to $16.8 million, supported by contracts from Eversource Energy and Boston public school projects. Orion reported a full-year net loss of $11.8 million, or ($0.36) per share, flat compared to FY’24.

Looking ahead, Orion projects FY’26 revenue of approximately $84 million. This represents 5% year-over-year growth—fueled by a $7 million EV charging backlog and several long-term LED lighting and maintenance contracts.

Analyst Reaffirms Buy Following Q4 Miss and FY’26 Outlook

- HC Wainwright & Co. analyst Amit Dayal maintained a Buy rating but lowered the price target from $3 to $2.

Which Analyst has the best track record to show on OESX?

Analyst Amit Dayal (HC WAINWRIGHT) currently has the highest performing score on OESX with 4/10 (40%) price target fulfillment ratio. His price targets carry an average of $1.91 (175.23%) potential upside. Orion Energy Systems stock price reaches these price targets on average within 166 days.

Daily stock Analysts Top Price Moves Snapshot