Selected stock price target news of the day - November 25th, 2024

By: Matthew Otto

Elastic Exceeds Q2 Expectations and Raises FY2025 Guidance Amid Cloud Growth

Elastic N.V. delivered its results for the second quarter of fiscal 2025 reporting earnings per share (EPS) of $0.59, outperforming the analyst estimate of $0.38 by $0.21. Total revenue for the quarter reached $365 million, surpassing the consensus estimate of $354.3 million and reflecting an 18% year-over-year growth – 17% in constant currency.

Elastic Cloud revenue was a driver, increasing 25% year-over-year to $169 million. Elastic achieved a non-GAAP operating income of $64 million with an 18% margin, while cash, cash equivalents, and marketable securities totaled $1.198 billion. Key customer metrics also improved, with customers generating over $100,000 in annual contract value increasing to over 1,420, and the subscription customer base growing to approximately 21,300.

For Q3 FY2025, Elastic projects EPS of $0.46 to $0.48, above the consensus of $0.41, and revenue of $367 to $369 million, exceeding the consensus of $366.7 million. For FY2025, Elastic anticipates EPS of $1.68 to $1.72, ahead of the consensus of $1.53, and revenue of $1.451 to $1.457 billion, surpassing the $1.442 billion consensus.

Analysts Respond Positively to Performance with Upgrades and Target Increases

- Wedbush analyst Daniel Ives upgraded from Neutral to Outperform with a price target of $135.

- DA Davidson analyst Gil Luria maintained a Neutral rating but raised the price target from $75 to $115.

- Scotiabank analyst Patrick Colville maintained a Sector Outperform rating while lifting the price target from $92 to $135.

- Truist Securities analyst Joel Fishbein reiterated a Buy rating and boosted the price target from $105 to $135.

- Guggenheim analyst Howard Ma kept a Buy rating and increased the price target from $100 to $120.

- Jefferies analyst Brent Thill maintained a Buy rating and raised the price target from $110 to $135.

- Canaccord Genuity analyst Kingsley Crane remained with a Buy rating and elevated the price target from $110 to $130.

- Piper Sandler analyst Rob Owens maintained an Overweight rating and lifted the price target from $100 to $130.

- RBC Capital analyst Matthew Hedberg held an Outperform rating and raised the price target from $110 to $130.

- Stifel analyst Brad Reback reiterated a Buy rating while increasing the price target from $98 to $132.

- Goldman Sachs analyst Kash Rangan retained a Neutral rating but lifted the price target from $99 to $113.

- JP Morgan analyst Pinjalim Bora maintained an Overweight rating and raised the price target from $100 to $130.

- Wells Fargo analyst Andrew Nowinski kept an Overweight rating and raised the price target from $100 to $135.

- Oppenheimer analyst Ittai Kidron reiterated an Outperform rating and increased the price target from $125 to $140.

Which Analyst has the best track record to show on ESTC?

Analyst John Difucci (GUGGENHEIM) currently has the highest performing score on ESTC with 6/6 (100%) price target fulfillment ratio. His price targets carry an average of $25.54 (34.30%) potential upside. Elastic N.V. stock price reaches these price targets on average within 25 days.

Intuit Delivers Strong Q1 Results but Issues Cautious Q2 Outlook

Intuit delivered its financial results for Q1 FY2025, which ended October 31, 2024, showcasing a rise of total revenue for 10% year-over-year to $3.3 billion, exceeding LSEG’s consensus estimate of $3.14 billion. Adjusted earnings per share (EPS) were $2.50, surpassing expectations of $2.35.

Net income declined to $197 million, or $0.70 per share, compared to $241 million, or $0.85 per share, in Q1 FY2024. Growth was primarily driven by the Global Business Solutions Group, which saw a 9% revenue increase to $2.5 billion, and Credit Karma, which reported a 29% revenue surge to $524 million. Meanwhile, the Consumer Group faced a 6% revenue decline, attributed to the prior year’s extended California tax filing deadline.

Intuit reaffirmed its FY2025 guidance, projecting revenue between $18.16 billion and $18.35 billion, implying 12% to 13% growth. Adjusted EPS for the year is expected to range from $19.16 to $19.36, reflecting a 13% to 14% increase.

For Q2 FY2025, revenue is forecasted between $3.81 billion and $3.85 billion, below analysts’ expectations of $3.87 billion, due to timing adjustments from TurboTax desktop software promotions. Despite this, full-year revenue expectations remain unaffected.

Intuit continues to invest in AI-driven innovation to strengthen its offerings, particularly in QuickBooks and Mailchimp. Intuit also repurchased $570 million in stock during the quarter, leaving $4.3 billion in authorization, and announced a 16% increase in its quarterly dividend to $1.04 per share.

Analyst Ratings Reflect Mixed Reactions to Q1 FY2025 Results

- Jefferies analyst Brent Thill maintained a Buy rating while raising the price target from $790 to $800.

- RBC Capital analyst Rishi Jaluria reiterated an Outperform rating and the price target at $760.

- Stifel analyst Brad Reback maintained a Buy rating but lowered the price target from $795 to $725.

- JP Morgan analyst Mark Murphy upheld a Neutral stance and increased the price target from $600 to $640.

- Oppenheimer analyst Scott Schneeberger continued with an Outperform rating and raised the price target from $712 to $722.

- Barclays analyst Raimo Lenschow reaffirmed an Overweight rating but trimmed the price target from $800 to $775.

- Morgan Stanley analyst Keith Weiss maintained an Equal-Weight rating yet raised the price target from $685 to $730.

Which Analyst has the best track record to show on INTU?

Analyst Keith Weiss (MORGAN STANLEY) currently has the highest performing score on INTU with 22/27 (81.48%) price target fulfillment ratio. His price targets carry an average of $82.18 (12.69%) potential upside. Intuit stock price reaches these price targets on average within 101 days.

NetApp Reports Q2 Results with All-Flash Array Growth and Raises Financial Outlook for FY2025

NetApp reported its financial results for the second quarter of fiscal year 2025, with net revenues of $1.66 billion, reflecting a 6% year-over-year increase. This performance was driven by an annualized net revenue run rate of $3.8 billion in all-flash arrays, up 19% from the previous year.

Additionally, NetApp saw a 43% year-over-year growth in its first-party and marketplace cloud storage services revenue. NetApp’s operating margins also showed improvement, with a GAAP operating margin of 21% and a non-GAAP operating margin of 29%. NetApp reported a GAAP net income of $299 million, or $1.42 per share, and non-GAAP net income of $392 million, or $1.87 per share. NetApp returned $406 million to shareholders through share repurchases and dividends.

Looking ahead, NetApp has raised its financial guidance for the third quarter of fiscal 2025, forecasting net revenues between $1.61 billion and $1.76 billion and adjusted earnings per share in the range of $1.85 to $1.95. For the full fiscal year, NetApp expects net revenues between $6.54 billion and $6.74 billion, with adjusted earnings per share between $7.20 and $7.40.

Analysts expressed optimism, with Evercore ISI analyst Amit Daryanani, raising its price target from $130 to $140, citing strong revenue growth, margin performance, and NetApp’s strategic diversification across cloud, on-premises, and as-a-service offerings.

Analysts Raise Price Targets Following Q2 Results

- Citigroup analyst Asiya Merchant maintained a Neutral rating and increased the price target from $130 to $135.

- TD Cowen analyst Karl Ackerman maintained a Buy rating and lifted the price target from $145 to $160.

- Stifel analyst Matthew Sheerin kept a Buy rating while raising the price target from $140 to $145.

- Wells Fargo analyst Aaron Rakers reiterated an Equal-Weight rating and boosted the price target from $135 to $140.

- Barclays analyst Tim Long held an Equal-Weight rating and raised the price target from $119 to $132.

- Morgan Stanley analyst Meta Marshall kept an Equal-Weight rating and adjusted the price target from $127 to $132.

- Northland Capital Markets analyst Nehal Chokshi kept a Market Perform rating and increased the price target from $108 to $120.

- BofA Securities analyst Wamsi Mohan maintained an Underperform rating, but raised the price target from $115 to $121.

Which Analyst has the best track record to show on NTAP?

Analyst Karl Ackerman (TD COWEN) currently has the highest performing score on NTAP with 10/13 (76.92%) price target fulfillment ratio. His price targets carry an average of $35.01 (28.01%) potential upside. NetApp stock price reaches these price targets on average within 154 days.

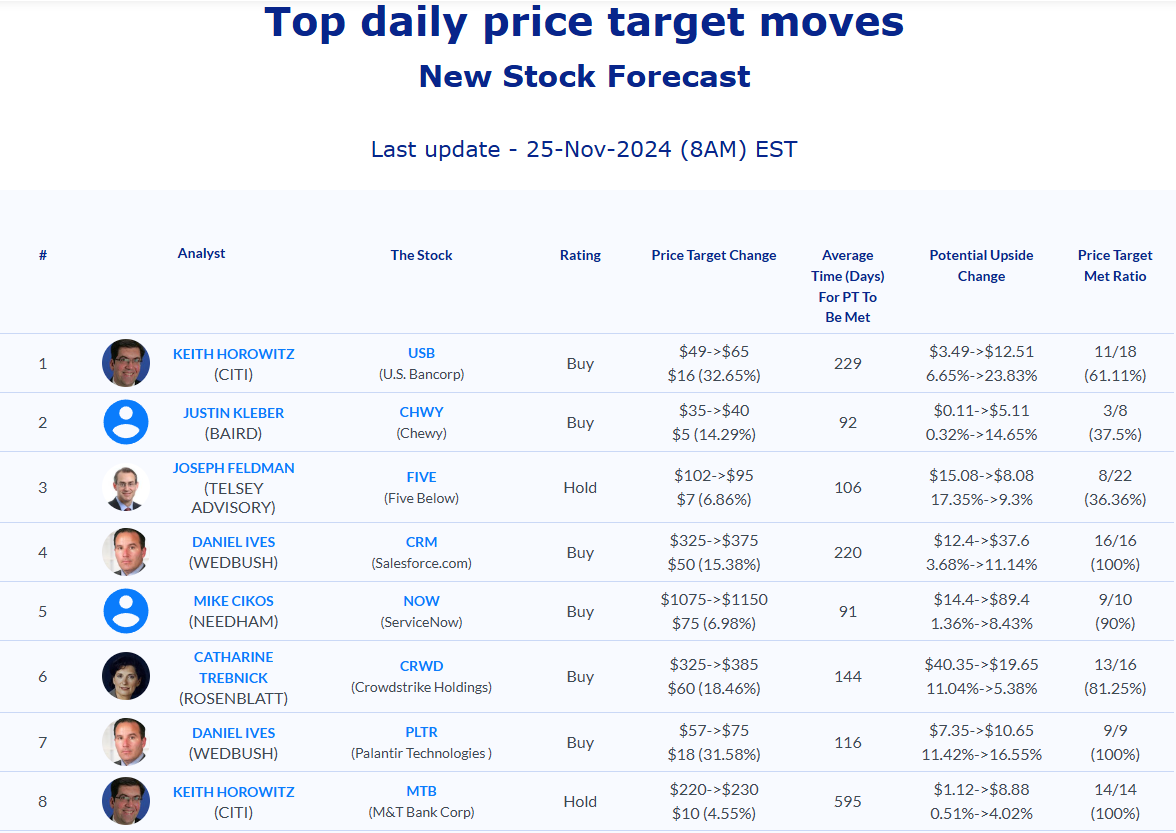

Daily stock Analysts Top Price Moves Snapshot