Selected stock price target news of the day - October 14th, 2025

By: Matthew Otto

Domino’s Pizza Posts Q3 2025 Results with Moderate Sales Growth and Earnings Beat

Domino’s Pizza reported third-quarter results for 2025, surpassing Wall Street expectations. The company posted earnings per share (EPS) of $4.08, exceeding analyst estimates of $3.96 by $0.12. Revenue for the quarter reached $1.15 billion, slightly ahead of the $1.14 billion consensus forecast.

Global retail sales increased 6.3% excluding foreign currency impact, driven by steady gains in both domestic and international markets. U.S. same-store sales rose 5.2%, while international same-store sales grew 1.7%.

Domino’s also achieved global net store growth of 214 locations, including 29 new stores in the U.S. and 185 abroad. Income from operations improved 12.2% to $223.2 million, reflecting stronger margins and efficiency in the supply chain segment.

Net income declined 5.2% to $139.3 million due to unrealized losses from the company’s investment in DPC Dash Ltd. Domino’s maintained strong cash generation, producing $552.3 million in operating cash flow and $495.6 million in free cash flow through the first three quarters of 2025—up 31.8% year-over-year. The company repurchased $74.7 million of common stock during the quarter and completed a $1 billion refinancing to reinforce its capital structure.

TD Cowen Reaffirms Rating and Price Target on Domino’s Pizza

- TD Cowen analyst Andrew M. Charles reiterated a Buy rating and a $510 price target.

Which Analyst has the best track record to show on DPZ?

Analyst Brian Mullan (PIPER SANDLER) currently has the highest performing score on DPZ with 18/19 (94.74%) price target fulfillment ratio. His price targets carry an average of $36.63 (9.01%) potential upside. Domino’s Pizza stock price reaches these price targets on average within 132 days.

Broadcom Introduces Wi-Fi 8 Silicon to Support Billions of AI-Connected Devices Worldwide

Broadcom has introduced the industry’s first Wi-Fi 8 silicon solutions, targeting the rapidly expanding AI-driven connectivity market that is projected to exceed 30 billion connected devices globally by 2030, according to IDC estimates.

The new chips—BCM6718, BCM43840, BCM43820, and BCM43109—address diverse use cases across over 1.5 billion households and enterprises relying on Wi-Fi connectivity. Built on the IEEE 802.11bn standard, Wi-Fi 8 is engineered for high-throughput, low-latency communication and up to 30% higher energy efficiency compared to Wi-Fi 7.

With features such as Coordinated Beamforming, Dynamic Sub-Channel Operation, and Extended Long Range (ELR), the new silicon can deliver consistent multi-gigabit speeds and stable connections across dense and demanding environments, supporting the bandwidth required for AI workloads, smart home systems, and enterprise edge applications.

Broadcom’s Wi-Fi 8 family integrates a hardware-accelerated telemetry engine that enables real-time analytics across millions of connected nodes, optimizing Quality of Experience (QoE) and reducing maintenance costs through AI-driven automation.

Broadcom’s decision to license its Wi-Fi 8 intellectual property is expected to accelerate adoption in the IoT, automotive, and mobile sectors, which together represent an estimated 18 billion active wireless devices worldwide. Technology partners, including ASUS, NETGEAR, and Comcast, plan to roll out Wi-Fi 8-enabled products beginning in 2026.

Analysts Reaffirm Buy Ratings on Broadcom as Price Targets Rise by an Average of 14%

- Deutsche Bank analyst Ross Seymore maintained a Buy rating and raised the price target from $350 to $400.

- Morgan Stanley analyst Joseph Moore kept a Buy rating and increased the price target to $409.

- UBS analyst Timothy Arcuri upheld a Buy rating but lifted the price target from $365 to $415.

Which Analyst has the best track record to show on AVGO?

Analyst Joseph Moore (MORGAN STANLEY) currently has the highest performing score on AVGO with 11/12 (91.67%) price target fulfillment ratio. His price targets carry an average of $47.68 (14.26%) potential upside. Broadcom stock price reaches these price targets on average within 144 days.

Nurix Therapeutics Posts Q3 Loss and Updates on Bexobrutideg Clinical Plans

Nurix Therapeutics reported its third-quarter 2025 results, posting an EPS of ($1.03), which was $0.20 below analyst expectations, and revenue of $7.89 million, falling short of the consensus estimate of $16.05 million.

Revenue declined from $12.6 million a year earlier, primarily due to the completion of certain Sanofi research programs, partly offset by ongoing collaboration activities with Pfizer. Research and development expenses increased to $86.1 million from $55.5 million, reflecting higher clinical and manufacturing costs tied to advancing the company’s lead program, bexobrutideg. General and administrative expenses rose to $13.2 million, while the company ended the quarter with $428.8 million in cash and marketable securities.

Nurix plans to initiate pivotal trials of bexobrutideg in relapsed or refractory chronic lymphocytic leukemia (CLL) in the second half of 2025. CLL affects an estimated 195,000 people in the United States, with roughly 20,000 new cases diagnosed each year, many of whom develop resistance to current BTK inhibitors.

In a Phase 1a study, bexobrutideg showed an 80.9% overall response rate (ORR) among 47 evaluable patients, including one complete response and a median time to first response of 1.9 months. In Waldenström macroglobulinemia, a rare cancer that affects about 3 in every 1 million people, bexobrutideg achieved an 84.2% ORR among 19 participants, suggesting potential benefit for patients with limited treatment options.

At the EADV 2025 Congress, Nurix and Gilead presented preclinical results for GS-6791, an investigational IRAK4 degrader that demonstrated strong pathway inhibition and improved outcomes in dermatitis models—a condition affecting over 230 million people globally.

Analyst Lowers Price Target on Nurix While Maintaining Buy Rating

- HC Wainwright & Co. analyst Robert Burns maintained a Buy rating but lowered the price target from $34 to $33.

Which Analyst has the best track record to show on NRIX?

Analyst Terence Flynn (MORGAN STANLEY) currently has the highest performing score on NRIX with 4/5 (80%) price target fulfillment ratio. His price targets carry an average of $3.85 (31.69%) potential upside. Nurix Therapeutics stock price reaches these price targets on average within 162 days.

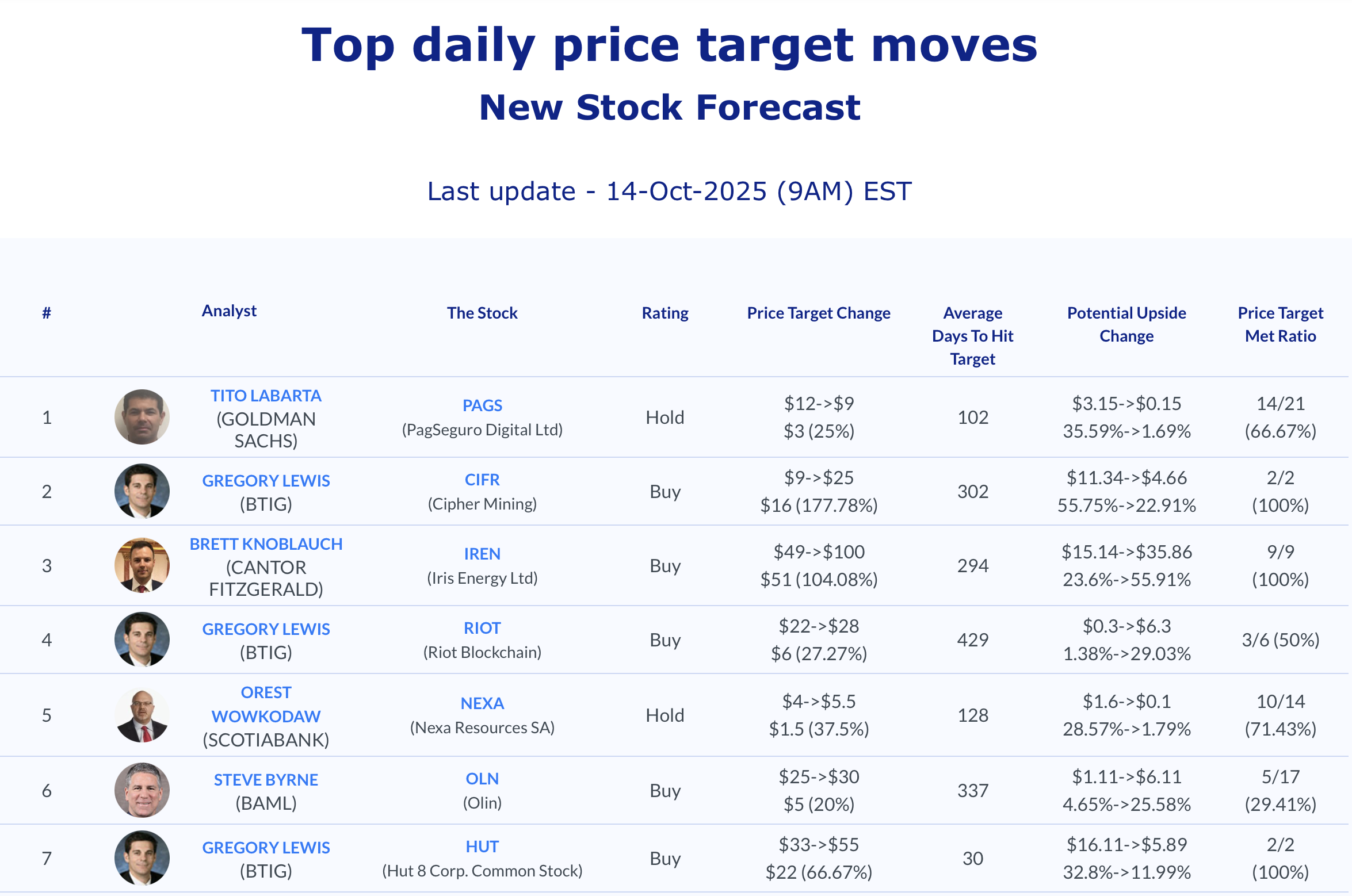

Daily Stock Analysts Top Price Moves Snapshot