Selected stock price target news of the day - June 02, 2023

By Matthew Otto

MongoDB’s Q1 2024 Earnings Beat Expectations with 29% Revenue Surge

The financial results of MongoDB for the first quarter of fiscal 2024 revealed strong performance with significant growth. The company reported total revenue of $368.3 million, reflecting a 29% increase year-over-year (versus the predicted $347 million. Atlas revenue in particular witnessed a 40% growth and the company added more customers than anticipated over the past two years.

In terms of financial highlights, the gross profit was $270.8 million, indicating a gross margin of 74%, slightly up from 73% in the previous year. The loss from operations was lesser this quarter ($68.5 million) compared to the same period in the previous year ($75.9 million). MongoDB’s net loss stood at $54.2 million, lower than the previous year’s net loss of $77.3 million.

The adjusted earnings were 56 cents per share, a significant beat compared to the 19 cents per share that was anticipated by analysts, according to Refinitiv.

Net loss for the quarter was $54 million, or 77 cents per share, which is an improvement over the net loss of $77 million, or $1.14 per share, from the same quarter in the previous year.

MongoDB had $1.9 billion in cash and equivalents, and generated $53.7 million of cash from operations in this quarter, up from $11.6 million in the same quarter of the previous year.

Business highlights included extending a strategic partnership with Alibaba through 2027 and an impressive record of over 150,000 banking transactions per second processed on the Temenos Banking Cloud using MongoDB Atlas.

Price Targets Increased Across the Board

- Analyst Miller Jump at Truist Securities reiterated a Buy rating and escalated the price target from $235 to $365.

- Matthew Broome at Mizuho sustained a Neutral rating while lifting the price target from $180 to $220.

- Ittai Kidron of Oppenheimer preserved an Outperform rating and elevated the price target from $270 to $430.

- Needham’s Mike Cikos held onto a Buy rating and boosted the price target from $250 to $430.

- William Power at Baird retained an Outperform rating and hiked the price target from $290 to $390.

- Citigroup’s Tyler Radke kept a Buy rating and amplified the price target from $363 to $430.

- Raimo Lenschow at Barclays persisted with an Overweight rating and increased the price target from $280 to $374.

- Patrick Walravens of JMP Securities sustained a Market Outperform rating and heightened the price target from $245 to $370.

- Kash Rangan at Goldman Sachs adhered to a Buy rating and raised the price target from $280 to $420.

- Brent Bracelin from Piper Sandler maintained an Overweight rating and advanced the price target from $270 to $400.

- Karl Keirstead of UBS elevated the price target to $425.

- Rishi Jaluria at RBC Capital raised the price target to $400.

The stock has not moved much in the last year with some analysts having a reserved look such as Howard Ma of Guggenheim.

Analyst Brent Bracelin has currently the highest performing score on MDB with 19/23 (82.61%) price target fulfillment ratio. His price targets carry on average an $47.18 (21.27%) potential upside and are fulfilled within average of 74 days.

Dollar General Adjusts Fiscal Year Guidance

Dollar General has reported its financial results for the first quarter of fiscal 2023, ending May 5, 2023, revealing a mixed performance.

Key highlights include:

- Net sales increased by 6.8%.

- Same-store sales saw a moderate increase of 1.6%.

- Operating profit decreased slightly by 0.7%, amounting to $740.9 million.

- Diluted Earnings Per Share (EPS) declined by 2.9% to $2.34.

- Cash flows from operations stood at $191 million.

However, Dollar General also adjusted its financial guidance for fiscal year 2023 due to a more challenging macroeconomic environment than previously anticipated. The company now expects:

- Net sales growth in the range of approximately 3.5% to 5.0%, compared to its previous expectation of 5.5% to 6%.

- Same-store sales growth in the range of approximately 1.0% to 2.0%, compared to its previous expectation of 3.0% to 3.5%.

- Diluted EPS in the range of an approximate 8% decline to flat, compared to its previous expectation of growth of approximately 4% to 6%.

Dollar General also intends to reduce the number of expected new store openings in the pOpshelf format in 2023, now expecting 3,110 real estate projects in the United States, down from the previous expectation of 3,170 projects.

CEO Jeff Owen cited lower tax refunds and bad weather in March and April as some of the reasons for the weaker-than-expected sales. He also acknowledged the adverse impact of the macroeconomic environment, particularly on the company’s core customer base.

Wall Street Action

- Kelly Bania from BMO Capital maintains a Market Perform rating but revises the price target downwards from $230 to $175.

- Scot Ciccarelli from Truist Securities sustains a Hold rating and decreases the price target from $214 to $166.

- Karen Short from Credit Suisse keeps a Neutral rating and lowers the price target from $220 to $170.

- Bobby Griffin from Raymond James persists with a Strong Buy rating but trims the price target from $255 to $200.

- Edward Kelly from Wells Fargo maintains an Overweight rating and cuts the price target from $245 to $178.

- Robert Ohmes from B of A Securities continues with an Underperform rating and reduces the price target from $190 to $155.

- Rupesh Parikh from Oppenheimer retains an Outperform rating and brings down the price target from $240 to $200.

- Krisztina Katai from Deutsche Bank upholds a Buy rating and adjusts the price target downwards from $256 to $201.

- Joseph Feldman from Telsey Advisory Group reiterates an Outperform rating and sustains a $242 price target.

- Peter Keith from Piper Sandler downgrades Dollar General from Overweight to Neutral and drops the price target from $275 to $178.

The decline in the stock price has caught all the analysts by surprise as they all had substantial upside views prior to yesterday.

Analyst Kelly Bania of BMO has currently the highest performing score on DG with 11/15 (73.33%) price target fulfillment ratio. Her price targets carry on average an $17.22 (11.62%) potential upside and are fulfilled within average of 223 days.

Zscaler’s Q3 2023 Revenue Jumps 46% YoY to $418.8 Million

Zscaler announced strong Q3 2023 financial results, ended on April 30, 2023, with significant increases in several key metrics:

- Revenue: Grew by 46% year-over-year, reaching $418.8 million.

- Calculated Billings: Rose by 40% year-over-year, amounting to $482.3 million.

- Deferred Revenue: Increased by 44% year-over-year, totaling $1,175.4 million.

- GAAP Net Loss: Improved from a loss of $101.4 million to a loss of $46.0 million year-over-year.

- Non-GAAP Net Income: Increased from $24.7 million to $74.6 million year-over-year.

Looking ahead, for the fourth quarter of fiscal 2023, Zscaler expects:

- Revenue: $429 million to $431 million.

- Non-GAAP income from operations: $69 million to $70 million.

- Non-GAAP net income per share: Approximately $0.49.

For the full fiscal year 2023, Zscaler expects:

- Revenue: Approximately $1.591 billion to $1.593 billion.

- Calculated billings: $1.974 billion to $1.978 billion.

- Non-GAAP income from operations: $224 million to $225 million.

- Non-GAAP net income per share: $1.63 to $1.64.

Zscaler Q3 2023 Results Elicit Upward Price Target Revisions by Analysts

- Stifel’s Adam Borg maintains a Buy rating on Zscaler, raising the price target from $135 to $150.

- Scotiabank’s Patrick Colville holds a Sector Outperform position, lifting the price target from $138 to $150.

- Evercore ISI Group’s Peter Levine maintains an Outperform rating, increasing the price target from $165 to $170.

- Loop Capital’s Yun Kim keeps a Hold rating, raising the price target from $125 to $135.

- BMO Capital’s Keith Bachman sustains an Outperform position, upping the price target from $120 to $150.

- Wells Fargo’s Andrew Nowinski persists with an Overweight stance, raising the price target from $156 to $175.

- RBC Capital’s Matthew Hedberg keeps an Outperform rating, with the price target lifted from $155 to $162.

- UBS’s Roger Boyd maintains a Buy rating, raising the price target from $170 to $175.

- Canaccord Genuity’s Michael Walkley keeps a Buy position, lifting the price target from $155 to $160.

- Barclays’ Saket Kalia continues with an Equal-Weight rating, upping the price target from $127 to $145.

Analyst Trevor Walsh of JMP has the current street high.

Analyst Alex Henderson of Needham has currently the highest performing score on ZS stock with 15/23 (65.22%) price target fulfillment ratio. His price targets carry on average an $46.04 (32.22%) potential upside and are fulfilled within an average of 69 days.

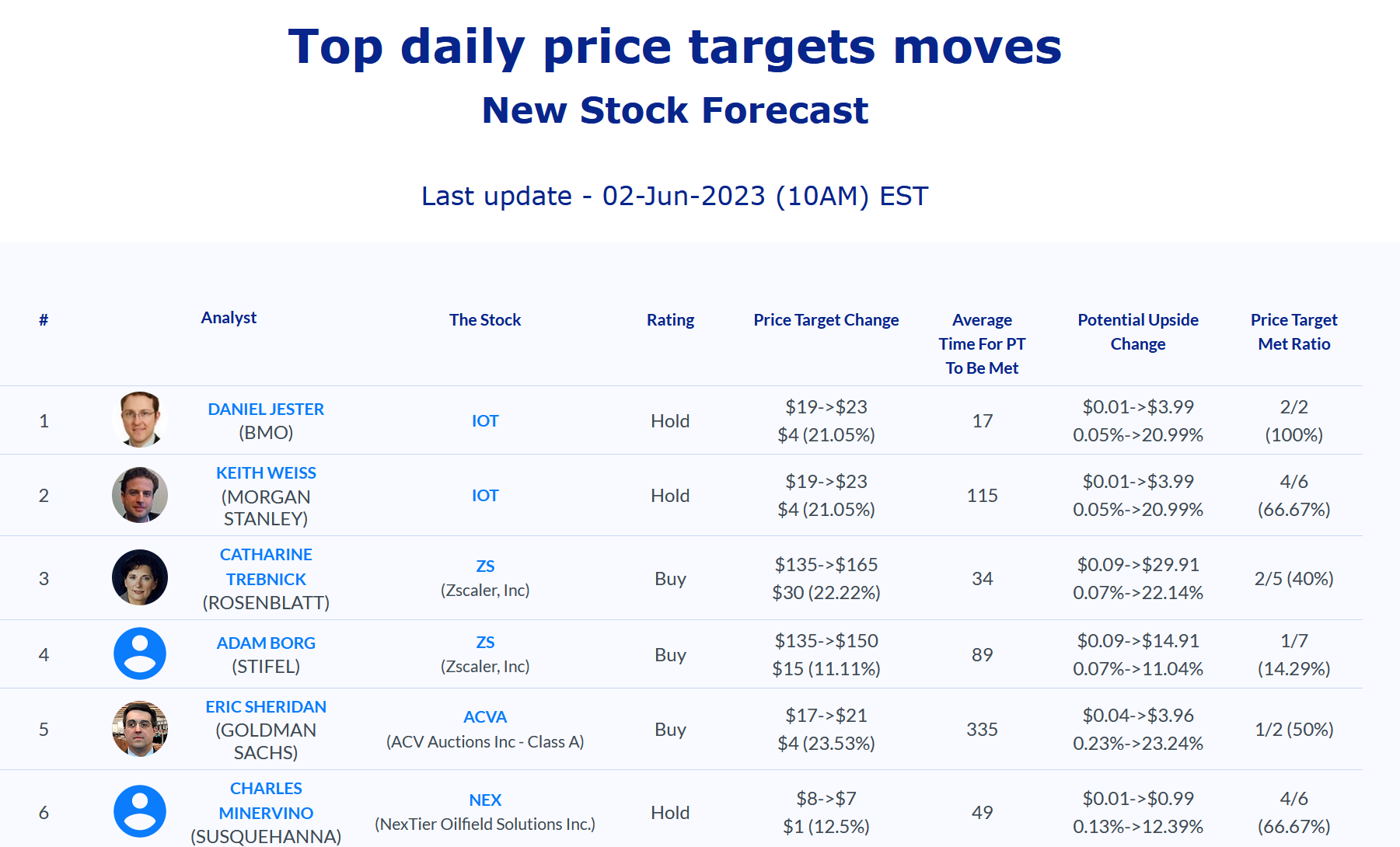

Daily stock Analysts Top Price Moves Snapshot