Selected stock price target news of the day - September 26th, 2025

By: Matthew Otto

CarMax Q2 Results Miss Analyst Expectations as Sales and Profit Decline

CarMax reported second-quarter results for the period ended August 31, 2025, missing Wall Street estimates on both earnings and revenue. The company posted earnings per diluted share of $0.64, $0.4 below the analyst consensus estimate of $1.04. Revenue came in at $6.59 billion, short of the $7.04 billion expected by analysts.

Retail used unit sales fell 5.4% while comparable store used unit sales declined 6.3%. Wholesale unit sales also decreased, down 2.2%. Retail used gross profit per unit was $2,216, wholesale profit per unit was $993, and Extended Protection Plan margin per unit was $576, each consistent with last year’s second quarter.

Total gross profit decreased 5.6% to $717.7 million, while SG&A expenses fell 1.6% to $601.1 million. CarMax Auto Finance (CAF) income dropped 11.2% to $102.6 million, as higher provisions for loan losses offset interest margin gains.

CarMax purchased 293,000 vehicles from consumers and dealers, down 2.4% from last year, with consumer-sourced vehicles accounting for 262,000 units. During the quarter, CarMax repurchased $180 million in stock and opened three new store locations and a reconditioning center. Management also announced plans to reduce SG&A by at least $150 million over the next 18 months.

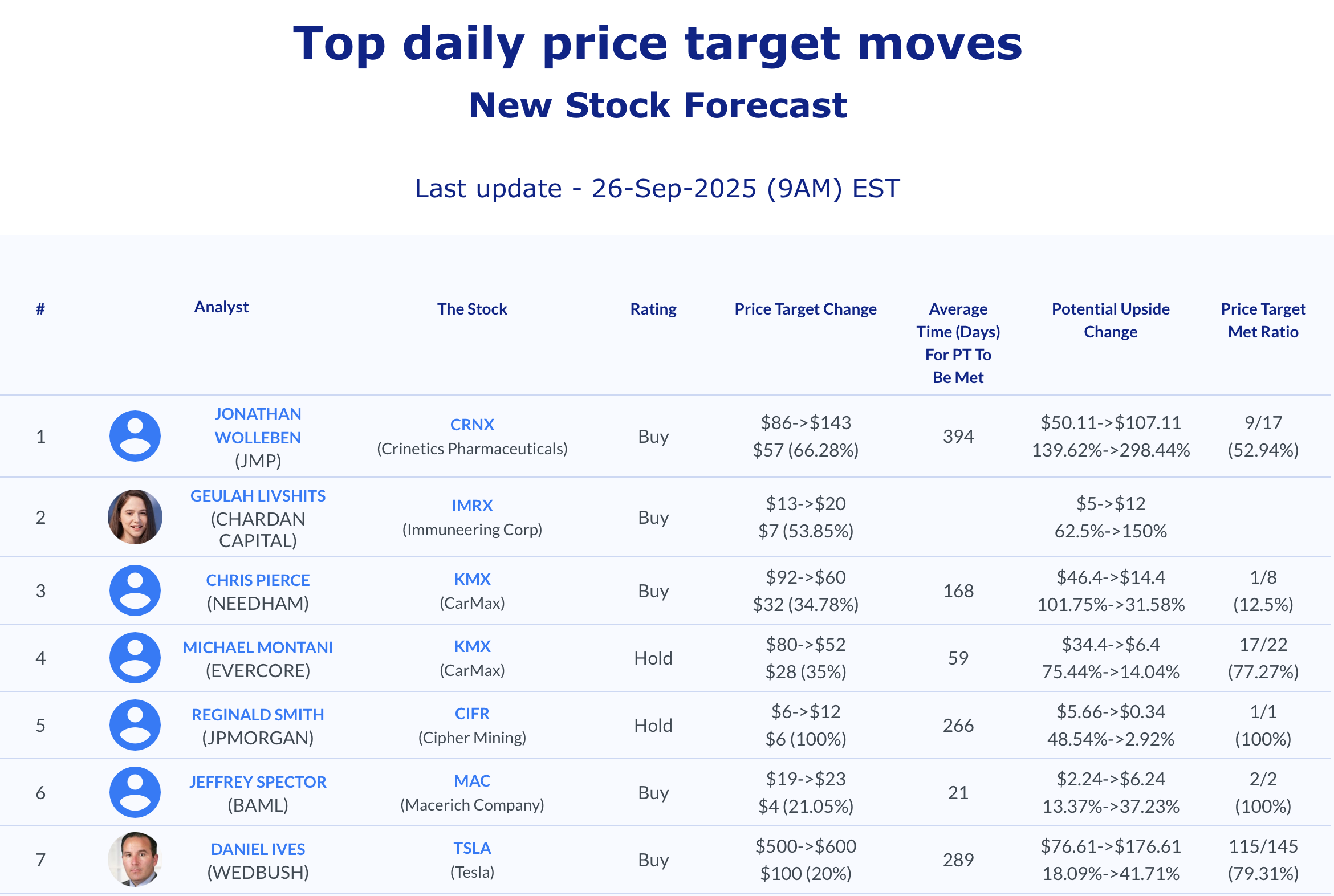

Analyst Ratings on CarMax Shift with Average Price Target Down 35%

- Evercore ISI Group analyst Michael Montani downgraded from Outperform to In-Line and the price target from $80 to $52.

- Needham analyst Chris Pierce maintained a Buy rating but reduced the price target from $92 to $60.

- Oppenheimer analyst Brian Nagel lowered from Outperform to Perform.

Which Analyst has the best track record to show on KMX?

Analyst Scot Ciccarelli (TRUIST) currently has the highest performing score on KMX with 26/28 (92.86%) price target fulfillment ratio. His price targets carry an average of $6.83 (10.17%) potential upside. CarMax stock price reaches these price targets on average within 89 days.

Costco Reports Higher Fourth-Quarter Earnings and Revenue Growth

Costco Wholesale reported fourth-quarter net sales of $84.4 billion, an increase of 8% from $78.2 billion a year earlier. Total revenue, which includes membership fees, reached $86.16 billion, compared with $79.7 billion in the prior-year quarter and slightly above the consensus estimate of $86.08 billion. Net income rose to $2.61 billion, or $5.87 per diluted share, up from $2.35 billion, or $5.29 per share, a year ago. Earnings per share came in $0.06 higher than the analyst estimate of $5.81.

For the fiscal year ended August 31, 2025, Costco posted net sales of $269.9 billion, an 8.1% increase from $249.6 billion the previous year, and total revenue of $275.2 billion. Annual net income was $8.1 billion, or $18.21 per diluted share, compared with $7.37 billion, or $16.56 per share, last year. Membership fee income for the quarter grew 14% to $1.72 billion, while for the year it reached $5.32 billion, up from $4.83 billion.

Comparable sales, excluding the impacts of gasoline price changes and foreign exchange, increased 6% in the U.S., 8.3% in Canada, and 7.2% in other international markets during the quarter. Companywide comparable sales rose 6.4%, while e-commerce sales grew 13.5%.

For the full year, comparable sales increased 7.6% and e-commerce revenue rose 16.1%, totaling more than $19.6 billion, or just over 7% of net sales. Global traffic rose 3.7% during the quarter, and average transaction size increased 2.6%. Costco ended the fiscal year with 914 warehouses worldwide, including 629 in the United States and Puerto Rico and 110 in Canada, and plans to open 35 additional locations in the next fiscal year.

Analyst Ratings on Costco Hold Steady While Price Targets Shift Lower by 1.1%

- Telsey Advisory Group analyst Joseph Feldman maintained an Outperform rating and the price target at $1,100.

- JP Morgan analyst Christopher Horvers continued an Overweight stance but lowered the price target from $1,160 to $1,050.

- Morgan Stanley analyst Simeon Gutman reiterated a positive outlook and raised the price target to $1,130.

- Evercore ISI analyst Greg Melich reduced the price target from $1,060 to $1,025.

Which Analyst has the best track record to show on COST?

Analyst Christopher Horvers (JPMORGAN) currently has the highest performing score on COST with 19/21 (90.48%) price target fulfillment ratio. His price targets carry an average of $182.55 (18.68%) potential upside. Costco Wholesale stock price reaches these price targets on average within 224 days.

TD SYNNEX Q3 2025 Results Exceed Analyst Estimates on Revenue and Earnings

TD SYNNEX reported fiscal third quarter results for the period ended August 31, 2025. Revenue was $15.65 billion, up 6.6% from $14.68 billion a year earlier and ahead of the consensus estimate of $15.11 billion. Billings totaled $22.73 billion compared to $20.28 billion last year, an increase of 12.1%.

Gross profit rose to $1.13 billion from $961 million, with gross margin improving to 7.22% from 6.54%. Operating income grew 26.7% to $383.7 million, while net income advanced 27% to $226.8 million. Reported earnings per share were $2.74, and adjusted earnings per share were $3.58, exceeding analyst expectations of $3.04 by $0.54. Cash provided by operations was $246 million versus $386 million in the prior year, while free cash flow came in at $214 million compared to $339 million.

By region, the Americas delivered $9.3 billion in revenue, up 2%, Europe contributed $5.2 billion, up 12.7%, and Asia-Pacific and Japan generated $1.2 billion, up 20.4%. Billings reached $14.2 billion in the Americas, $6.9 billion in Europe, and $1.7 billion in Asia-Pacific and Japan. Operating income stood at $284 million in the Americas, $70 million in Europe, and $30 million in Asia-Pacific and Japan. During the quarter, the company returned $210 million to shareholders through $174 million of share repurchases and $36 million in dividends.

For the fourth quarter of fiscal 2025, TD SYNNEX provided guidance of $16.5 billion to $17.3 billion in revenue, compared to the consensus estimate of $15.99 billion, and earnings per share of $3.45 to $3.95, versus the analyst consensus of $3.33.

Analyst Ratings on TD SYNNEX Raised With Average Price Target Up 6.5%

- Barclays analyst Tim Long maintained an Equal-Weight rating while increasing the price target from $140 to $164.

- BofA Securities analyst Ruplu Bhattacharya continued a Buy rating and raised the price target from $170 to $180.

Which Analyst has the best track record to show on SNX?

Analyst Ashish Sabadra (RBC) currently has the highest performing score on SNX with 13/15 (86.67%) price target fulfillment ratio. His price targets carry an average of $15.18 (10.13%) potential upside. TD SYNNEX stock price reaches these price targets on average within 84 days.

Daily Stock Analysts Top Price Moves Snapshot