Selected stock price target news of the day - May 6th, 2025

By: Matthew Otto

onsemi Reports 20% Revenue Decline as Free Cash Flow Rises 72% in First Quarter

onsemi reported first quarter 2025 revenue of $1,445.7 million, a decline from $1,862.7 million in the same quarter a year ago and $1,722.5 million in the previous quarter. Free cash flow reached $455 million, up 72% year-over-year and accounting for 31% of total revenue.

onsemi returned approximately $300 million to stockholders through share repurchases, representing 66% of its free cash flow. Cash from operations totaled $602 million, and net income stood at $231.6 million. It recorded a gross margin of 40% and an operating margin of 18.3%, both below the 45.9% and 29% reported in the first quarter of 2024.

Revenue by segment also showed year-over-year and sequential declines. Power Solutions Group (PSG) revenue fell to $645.1 million, down 26% year-over-year and 20% sequentially. Advanced Solutions Group (AMG) posted $566.4 million, down 19% from the prior year. Intelligent Sensing Group (ISG) reported $234.2 million, reflecting a 20% year-over-year drop.

For the second quarter of 2025, onsemi forecasts revenue between $1,400 million and $1,500 million. Expected gross margin is between 36.5% and 38.5%, with operating expenses ranging from $285 million to $300 million. Net other expense, including interest, is projected at $11 million.

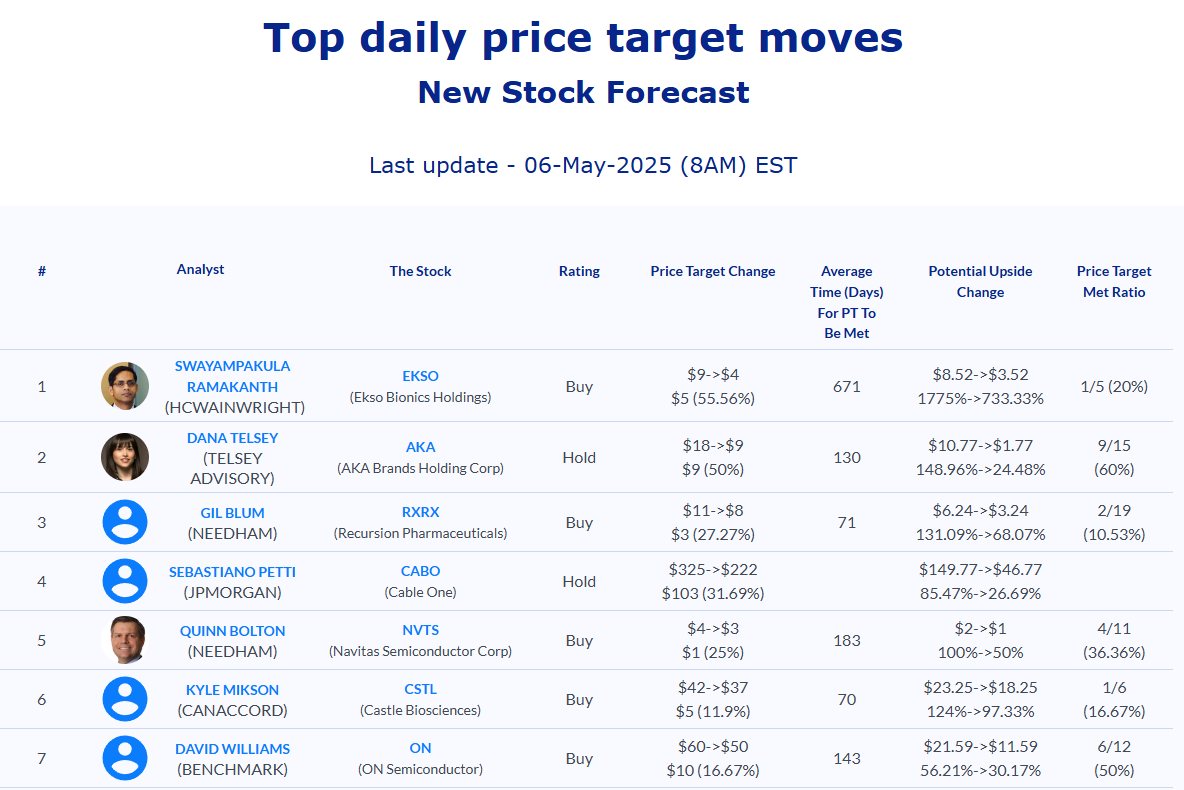

Analysts Lower Price Targets Following Q1 Results and Revenue Decline

- Benchmark analyst David Williams maintained a Buy rating but reduced the price target from $60 to $50.

- Needham analyst Quinn Bolton kept a Buy rating while trimming the price target from $57 to $50.

- Baird analyst Tristan Gerra lowered the price target from $42 to $34.

Which Analyst has the best track record to show on ON?

Analyst Anthony Stoss (CRAIG HALLUM) currently has the highest performing score on ON with 5/5 (100%) price target fulfillment ratio. His price targets carry an average of $2.07 (4.32%) potential upside. ON Semiconductor stock price reaches these price targets on average within 341 days.

BioCryst Posts Better-Than-Expected Q1 2025 Results and Raises Full-Year Revenue Guidance

BioCryst Pharmaceuticals reported total revenue of $145.5 million for the first quarter ended March 31, 2025, a 56.8% increase from $92.8 million in the same period last year. ORLADEYO® (berotralstat) net revenue totaled $134.2 million, up 51% from $88.9 million in Q1 2024, and exceeded the consensus estimate of $127.91 million. U.S. sales represented 89.5% of ORLADEYO revenue.

ORLADEYO is an oral, once-daily treatment to prevent hereditary angioedema (HAE) attacks. HAE is a rare genetic disorder that affects an estimated 1 in 50,000 people, or roughly 8,000 to 10,000 individuals in the U.S. alone. ORLADEYO offers a non-injectable option, with 84% of patients now on paid drug. BioCryst has filed to expand its use to children aged 2 to 11 via oral granules, which could extend access to a broader pediatric population.

BioCryst reported Q1 2025 earnings per share (EPS) of $0, $0.07 above the analyst estimate of ($0.07), compared to a net loss of $35.4 million, or ($0.17) per share, in Q1 2024. Operating income was $21.2 million, versus an operating loss of $14.5 million a year earlier. On a non-GAAP basis, operating income was $42.6 million, compared to a loss of $0.8 million.

Research and development expenses declined 19.8% year-over-year to $37.3 million, down from $46.5 million, primarily due to the discontinuation of the Factor D programs. Selling, general and administrative expenses increased 38.7% to $82.5 million, compared to $59.5 million in Q1 2024. Interest expense was $23.5 million, down 4.1% from $24.5 million. Cash, cash equivalents, restricted cash, and investments totaled $317.3 million as of March 31, 2025, compared to $338.4 million a year earlier. Net cash utilization in Q1 2025 was $25.5 million.

In April 2025, BioCryst repaid $75 million of Pharmakon debt, which is expected to reduce total interest expense by approximately $23.5 million over the life of the loan. For full year 2025, BioCryst raised its ORLADEYO revenue guidance to $580 to $600 million, above both the prior range of $535 to $550 million and the consensus estimate of $563.6 million. Projected operating expenses are $440 to $450 million, not including stock-based compensation.

Analysts Maintain Ratings, Adjust Price Targets Following Q1 2025 Results

- HC Wainwright & Co. analyst Andrew Fein reiterated with a Buy rating and a $30 price target.

- Needham analyst Serge Belanger maintained a Buy rating and raised the price target from $15 to $17.

Which Analyst has the best track record to show on BCRX?

Analyst Brian Abrahams (RBC) currently has the highest performing score on BCRX with 17/24 (70.83%) price target fulfillment ratio. His price targets carry an average of $4.18 (61.29%) potential upside. BioCryst Pharmaceuticals stock price reaches these price targets on average within 513 days.

Vertex Pharmaceuticals Reports Q1 2025 Financial Results and Revises Full-Year Revenue Guidance

Vertex Pharmaceuticals reported first-quarter 2025 revenue of $2.77 billion, falling short of the consensus estimate of $2.86 billion. Earnings per share (EPS) for the quarter were $4.06, missing the analyst estimate of $4.26 by $0.20.

Trikafta® / Kaftrio® sales reached $2.53 billion, reflecting a 2% increase from the same period in 2024. However, revenue outside the U.S. declined by 5% year-over-year, primarily due to lower sales in Russia.

Trikafta® (Kaftrio® in Europe) is a triple-combination therapy from Vertex Pharmaceuticals used to treat cystic fibrosis (CF), a genetic disease that affects around 92,000 people worldwide. The therapy targets the defective Cystic Fibrosis Transmembrane Conductance Regulator (CFTR) protein caused by gene mutations, particularly F508del. Trikafta® / Kaftrio® is approved for patients with at least one F508del mutation and can benefit approximately 90% of all CF patients.

For the full year, Vertex revised its 2025 revenue guidance to a range of $11.85 billion to $12 billion, up slightly from the previous estimate of $11.75 billion to $12 billion. Vetex’s total expenses for Q1 2025, which include research and development (R&D) and selling, general, and administrative (SG&A) costs, amounted to $2.6 billion, an increase from $2.2 billion in Q1 2024.

Analysts React to Q1 Miss and Outlook with Mixed Rating Changes

- Needham analyst Joseph Stringer maintained a Hold rating.

- Leerink Partners analyst David Risinger downgraded from Outperform to Market Perform and the price target from $550 to $503.

- Scotiabank analyst Greg Harrison lowered his price target to $442.

- Morgan Stanley analyst Terence Flynn raised the price target to $464.

Which Analyst has the best track record to show on VRTX?

Analyst Mohit Bansal (WELLS FARGO) currently has the highest performing score on VRTX with 16/18 (88.89%) price target fulfillment ratio. His price targets carry an average of $21.6 (4.93%) potential upside. Vertex Pharmaceuticals stock price reaches these price targets on average within 284 days.

Daily stock Analysts Top Price Moves Snapshot