HubSpot (HUBS): Earnings Beat but Analysts Cut Price Targets on Soft Guidance

HubSpot beat fourth-quarter 2025 earnings expectations but guided conservatively for 2026, prompting a broad wave of analyst price target cuts. Despite revenue growth of 20% year over year, the cautious outlook led analysts across more than a dozen firms to reduce their valuations. You can track all analyst ratings and price targets for HUBS on AnaChart.

HUBS: HubSpot Earnings Beat as Analysts Cut Price Targets Following Guidance

HubSpot reported fourth-quarter revenue of $846.7 million and earnings per share of $3.09, exceeding analyst expectations of approximately $830.7 million in revenue and $2.99 per share, according to the company’s earnings release. Revenue increased 20% year over year on an as-reported basis and 18% in constant currency, with subscription revenue rising 21% to $829.0 million.

HubSpot projected full-year 2026 revenue of $3.69 billion to $3.70 billion, representing 18% growth on an as-reported basis and 16% growth in constant currency, according to company disclosures. First-quarter revenue was guided to $862 million to $863 million, up 21% year over year as reported and above consensus estimates.

The company also announced that its board authorized a new $1 billion share repurchase program, according to Business Wire.

Analysts Adjust HubSpot Price Targets Following Earnings

- Joshua Reilly (Needham) lowered his price target to $300 from $700, while maintaining a Buy rating.

● Gray Powell (BTIG) reduced his price target to $330 from $485 and kept a Buy rating.

● Brent Bracelin (Piper Sandler) cut his price target to $280 from $400, maintaining an Overweight rating.

● Terry Tillman (Truist Securities) lowered his price target to $300 from $650 while reiterating a Buy rating.

● Taylor McGinnis (UBS Group) reduced her price target to $325 from $450, with her Buy rating unchanged.

● Clarke Jeffries (Cantor Fitzgerald) lowered his price target to $280 from $500 and maintained an Overweight rating.

● Rishi Jaluria (RBC Capital) downgraded the stock to Sector Perform from Outperform and reduced his price target to $189 from $322.

● Keith Weiss (Morgan Stanley) cut his price target to $290 from $375, maintaining an Overweight rating.

● Mark Murphy (JPMorgan) reduced his price target to $350 from $500 while maintaining an Overweight rating.

● Brad Zelnick (Deutsche Bank) lowered his price target to $285 from $385 and kept a Buy rating.

● Daniel Jester (BMO Capital) reduced his price target to $285 from $385, maintaining an Outperform rating.

● David Hynes (Canaccord Genuity) maintained a Buy rating and set a $485 price target.

Which Analyst Has the Current Best Track Record on HUBS?

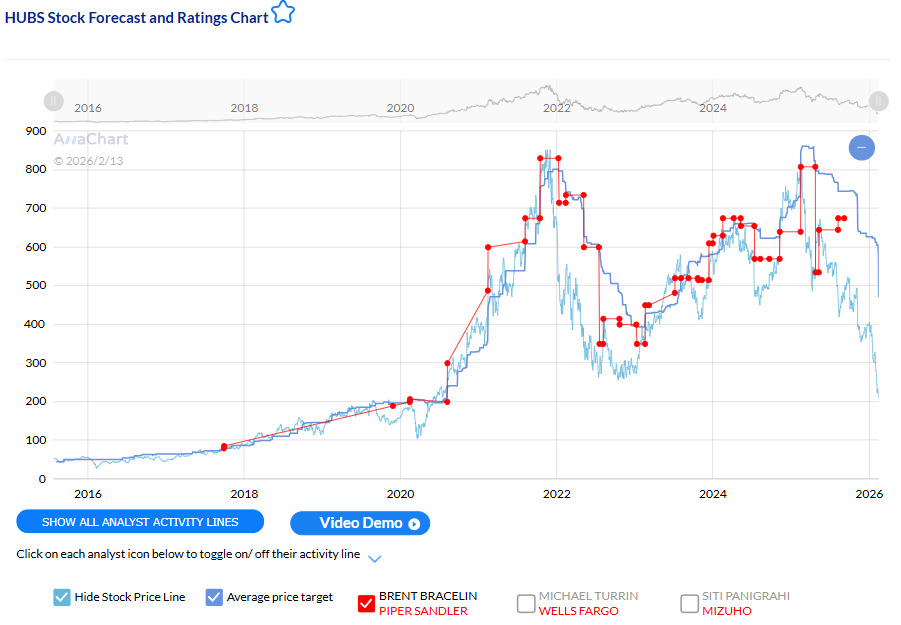

Among analysts tracked by AnaChart, Brent Bracelin (Piper Sandler) has one of the strongest track records on HubSpot, with a 94.12% price-target fulfillment ratio (32/34). His historical price targets have typically been reached within an average of 140 days.

Monday.com Earnings Beat Overshadowed by Weak Guidance as Analysts Cut Price Targets

Monday.com reported fourth-quarter revenue of $333.9 million and earnings per share of $1.04, exceeding analyst expectations of approximately $329.7 million in revenue and $0.91 per share, according to the company’s earnings release. Revenue increased 25% year over year, with full-year 2025 revenue reaching $1.232 billion, up 27% from the prior year.

Monday.com projected full-year 2026 revenue of $1.452 billion to $1.462 billion, representing 18% to 19% growth year over year, down from 27% growth in fiscal 2025 and below consensus estimates of $1.48 billion, according to company disclosures. First-quarter revenue was guided to $338 million to $340 million, below analyst estimates of $343 million.

During the earnings call, CFO Eliran Glazer said the company would no longer discuss previously provided 2027 targets, noting it would “revisit long-term targets when there is greater visibility and it’s appropriate to do so,” according to the earnings call transcript.

Analysts Adjust Monday.com Price Targets Following Earnings

- Keith Weiss (Morgan Stanley) maintained an Overweight rating and lowered his price target to $115 from $200.

- Michael Turrin (Wells Fargo) kept an Overweight rating and reduced his price target to $130 from $200.

- Clarke Jeffries (Cantor Fitzgerald) maintained an Overweight rating and lowered his price target to $95 from $148.

- Jackson Ader (KeyBanc) maintained an Overweight rating and reduced his price target to $140 from $220.

- Ken Wong (Guggenheim) has a Buy rating and lowered his price target to $180 from $250.

- Hannah Rudoff (Piper Sandler) maintained an Overweight rating and reduced her price target to $100 from $170.

- Allan Verkhovski (BTIG) maintained a Buy rating and lowered his price target to $135 from $210.

- Brad Sills (Bank of America) maintained a Neutral rating and reduced his price target to $95 from $157.

- Stephen Sheldon (William Blair) left an Outperform rating and trimmed his price target to $140 from $175.

- Tyler Radke (Citi) maintained a Buy rating and reduced his price target to $230 from $293.

- Alex Zukin (Wolfe Research) maintained an Outperform rating and set a $95 price target.

- Andrew Sherman (Loop Capital) set an $80 price target.

- Karl Keirstead (UBS) kept a Neutral rating and lowered his price target to $140 from $200.

- DJ Hynes (Canaccord Genuity) set a $140 price target.

- Brad Zelnick (Deutsche Bank) maintained a Buy rating and lowered his price target to $115 from $157.

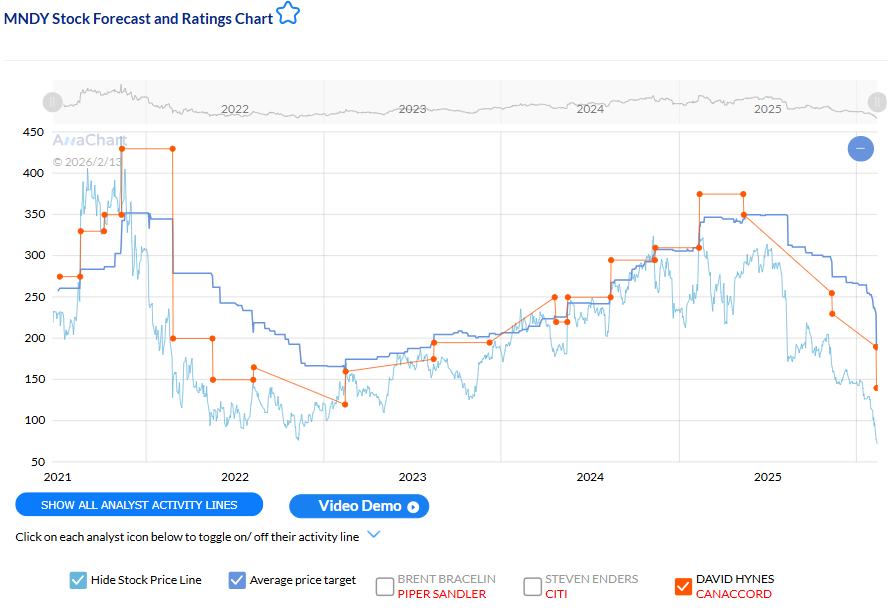

Which Analyst Has the Current Best Track Record on MNDY?

Among analysts tracked by AnaChart, David Hynes (Canaccord Genuity) has one of the strongest track records on monday.com, with a 75% price-target fulfillment ratio (12/16). His price targets have typically been reached within an average of 65 days.

Lyft Shares Fall After Revenue Miss and Weak Q1 Outlook Trigger Downgrades

Lyft reported fourth-quarter revenue of $1.59 billion, falling short of analyst expectations of $1.76 billion, according to the company’s earnings release. The company attributed the shortfall to a $168 million impact from legal, tax, and regulatory reserve changes and settlements. Excluding these items, revenue would have been $1.76 billion, according to company disclosures. Gross bookings of $5.1 billion grew 19% year over year, in line with analyst estimates.

Adjusted EBITDA increased 37% year over year to $154.1 million, exceeding analyst estimates of $147.7 million, according to company disclosures.

Lyft projected first-quarter adjusted EBITDA of $120 million to $140 million, below Wall Street expectations of $140.5 million, according to company disclosures. The company guided gross bookings to $4.86 billion to $5.00 billion for the first quarter, in line with analyst estimates.

Analysts Adjust Lyft Price Targets Following Earnings

- Justin Post (Bank of America) cut to Underperform from Buy and reduced his price target to $17 from $19.

- Brian Nowak (Morgan Stanley) kept an Equal Weight rating and lowered his price target to $17 from $22.50.

- John Colantuoni (Jefferies) maintained a Hold rating and reduced his price target to $15.50 from $20.

- Shyam Patil (Susquehanna) lowered his price target to $15 from $24, maintaining a Neutral rating.

- Ygal Arounian (CITI) sustained a Buy rating and reduced his price target to $30 from $32.

- Ken Gawrelski (Wells Fargo) leftb an Overweight rating yet lowered his price target to $18 from $20.

- Nikhil Devnani (Bernstein ) set a $23 price target while maintaining a Market Perform rating.

- Bernie McTernan (Needham) reiterated a Hold rating with no price target.

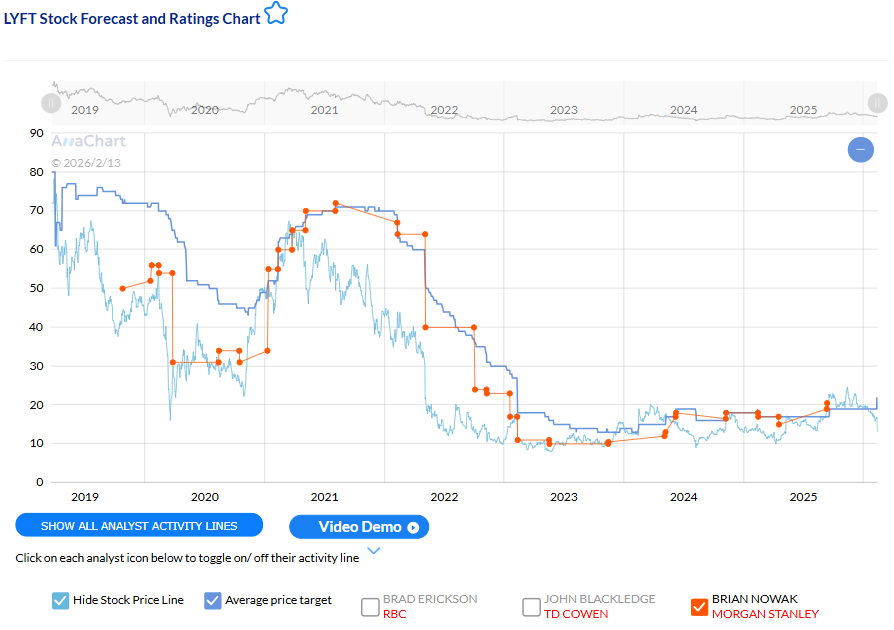

Which Analyst Has the Current Best Track Record on LYFT?

Among analysts tracked by AnaChart, Brian Nowak (Morgan Stanley) has one of the strongest track records on Lyft, with an 80% price-target fulfillment ratio (20/25). His price targets have historically been reached within an average of 184 days.