Analyst Price Target News: Week of February 26th, 2026

This week, analyst activity was driven by earnings releases across enterprise software, consumer discretionary, and home improvement. Workday’s disappointing FY2027 guidance triggered a broad wave of analyst price target cuts, while results from consumer names prompted mixed revisions across the sector.

By: Michael Muchugia

Workday Guidance Miss Triggers Broad Analyst Reset

Analysts responded to Workday’s fiscal fourth-quarter 2026 results with a sweeping round of price target cuts, as disappointing FY2027 subscription revenue guidance overshadowed a headline earnings beat and highlighted slower new business growth.

Workday reported non-GAAP EPS of $2.47 for the quarter, topping the consensus estimate of $2.32 by $0.15, while revenue of $2.53 billion edged past expectations of $2.52 billion, representing 14.5% year-over-year growth. Current remaining performance obligations reached $8.83 billion, up 15.8% year-over-year, beating estimates by approximately 0.2%.

Guidance for FY2027 subscription revenue came in below Street expectations, implying growth of approximately 12–13%, with management citing deal slippage across government and retail verticals and longer sales cycles among private equity-backed customers.

CEO Aneel Bhusri — who returned to lead the company following a management transition — emphasized that major AI firms run on Workday’s platform and reaffirmed the company’s agentic AI investment as a long-term growth driver. Needham maintained a Buy rating with a $300 price target, offering a counterbalance to the broader wave of revisions.

Analysts Adjust Workday Price Targets Following Earnings

Analyst revisions were overwhelmingly negative, with multiple firms issuing significant price target cuts and at least one outright downgrade following the guidance miss.

- Brent Thill (Jefferies) downgraded WDAY to Hold from Buy and slashed his price target to $150 from $325.

- Kirk Materne (Evercore ISI) downgraded WDAY to In Line from Outperform and lowered his price target to $160 from $200.

- J. Derrick Wood (TD Cowen) downgraded WDAY to Hold from Buy and lowered his price target to $155.

- Gil Luria (DA Davidson) maintained his rating and slashed his price target to $125 from $250.

- Jason Celino (KeyBanc) maintained an Overweight rating and lowered his price target to $155 from $260.

- Karl Keirstead (UBS) maintained his rating and lowered his price target to $130 from $170.

- Billy Fitzsimmons (Piper Sandler) maintained his rating and lowered his price target to $135.

- Robert Simmons (Rosenblatt) maintained a Buy rating and lowered his price target to $150.

- Ken Wong (Oppenheimer) maintained his rating and lowered his price target to $165.

- Keith Weiss (Morgan Stanley) maintained an Equal Weight rating and lowered his price target to $200 from $280.

- Michael Turrin (Wells Fargo) maintained an Overweight rating and lowered his price target to $180 from $255.

- Rishi Jaluria (RBC Capital) maintained an Outperform rating and lowered his price target to $180 from $220.

- Mark Murphy (JPMorgan) maintained an Overweight rating and lowered his price target to $190.

- Daniel Jester (BMO Capital) maintained an Outperform rating and lowered his price target to $182 from $204.

- Mark Marcon (Baird) maintained his rating and lowered his price target to $195.

- Raimo Lenschow (Barclays) maintained an Overweight rating and lowered his price target to $200 from $230.

- Mark Moerdler (Bernstein SocGen) maintained his rating and lowered his price target to $214 from $298.

- Scott Berg (Needham) maintained a Buy rating and kept his price target at $300.

More than 15 firms lowered price targets following the release, with multiple downgrades issued, indicating a broad recalibration of forward estimates.

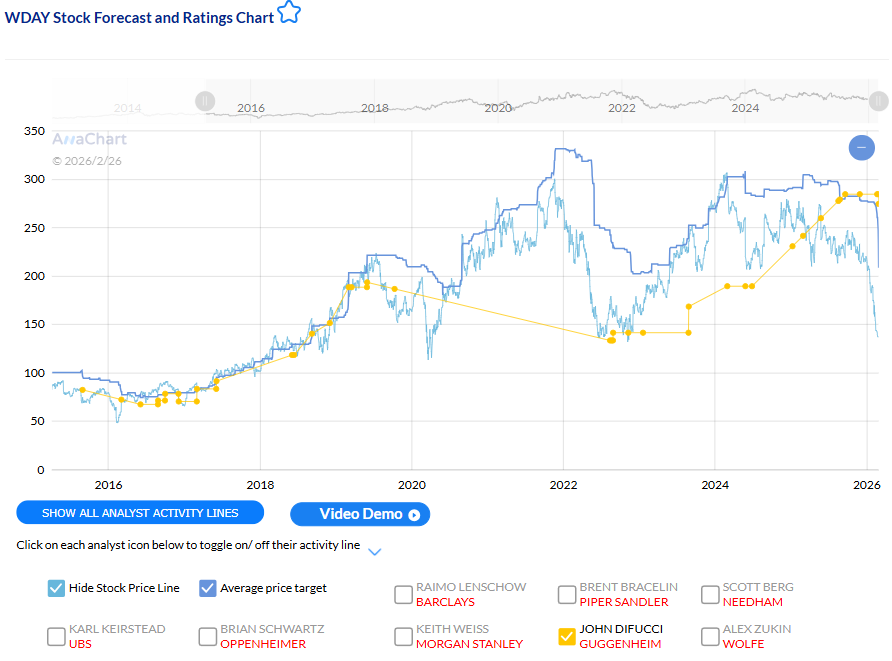

Which Analyst Has the Current Best Track Record on WDAY?

John DiFucci of Guggenheim currently ranks among the top performers on WDAY, with an 84.62% price target hit ratio across 26 predictions and an average time to target of 212 days, reflecting consistent alignment between target setting and price realization.

CAVA Crosses $1 Billion Revenue Milestone

CAVA delivered a quarter that exceeded expectations on nearly every front, with full-year revenue crossing $1 billion for the first time and 2026 guidance coming in ahead of analyst estimates, prompting a broad round of price target increases.

For the fourth quarter of 2025, CAVA reported revenue of $275.0 million, above analyst estimates, with adjusted EPS of $0.04 beating the consensus of $0.00. Same-restaurant sales grew 0.5%, supported by a 1.9% benefit from menu pricing and product mix, partially offset by a 1.4% decline in guest traffic. The company outlined plans to open 74 to 76 new restaurants in 2026, with a long-term target of more than 1,000 locations by 2032.

2026 same-store sales guidance of 3% to 5% came in ahead of prior analyst expectations, with early first-quarter trends tracking above the upper end of the range.

Analysts Adjust CAVA Price Targets Following Earnings

Revisions were uniformly upward, with analysts across multiple firms raising price targets in response to the earnings beat and stronger-than-expected guidance.

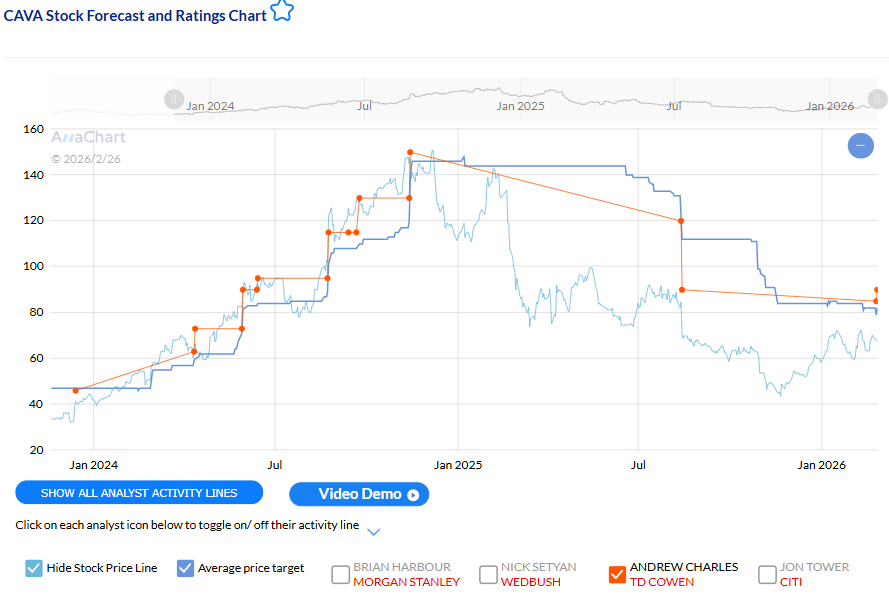

- Andrew Charles (TD Cowen) maintained a Buy rating and raised his price target to $90 from $85.

- Chris O’Cull (Stifel) maintained a Buy rating and lifted his price target to $90 from $75.

- Jake Bartlett (Truist Securities) maintained a Buy rating and raised his price target to $85 from $80.

- Brian Mullan (Piper Sandler) maintained his rating and raised his price target to $85 from $71.

- Sarang Vora (Telsey Advisory Group) maintained an Outperform rating and raised his price target to $88 from $85.

- Danilo Gargiulo (Bernstein SocGen) maintained his rating and raised his price target to $84 from $75.

- Dennis Geiger (UBS) maintained a Neutral rating and raised his price target to $75 from $69.

- Brian Vaccaro (Raymond James) reiterated a Market Perform rating.

Which Analyst Has the Current Best Track Record on CAVA?

Andrew Charles of TD Cowen currently ranks among the top performers on CAVA, with an 88.89% price target hit ratio across 9 predictions and an average time to target of 28 days, reflecting consistent alignment between target setting and price realization.

Home Depot Posts Largest EPS Beat in Years

Home Depot delivered its strongest earnings beat in multiple quarters with management providing cautious commentary on housing market conditions and large-ticket consumer demand.

The company reported fourth-quarter 2025 adjusted EPS of $2.72, topping the consensus estimate of $2.52 by $0.20, while revenue of $38.20 billion exceeded expectations of $38.01 billion. Transactions declined 1.6% in the quarter but were partially offset by a 2.4% rise in average ticket size. Home Depot also raised its quarterly dividend by approximately 1.3% to $2.33 per share, marking 39 consecutive years of dividend payments.

For FY2026, the company guided for total sales growth of 2.5% to 4.5%, comparable sales growth of flat to 2.0%, and adjusted EPS of $14.69 to $15.28. CEO Ted Decker cautioned that customers remain hesitant to commit to large-ticket projects amid affordability concerns, with housing turnover still well below long-term averages. Telsey Advisory Group analyst Joseph Feldman noted that the implied comparable sales figure at the midpoint of guidance would represent the strongest result in three years, with Home Depot’s continued share gains among professional customers cited as a structural positive.

Analysts Adjust Home Depot Price Targets Following Earnings

Analyst revisions were broadly constructive, with the majority of firms raising price targets in response to the earnings beat, though increases remained measured against a cautious macro backdrop.

- Michael Baker (DA Davidson) maintained a Buy rating and raised his price target to $445 from $407.

- Jonathan Matuszewski (Jefferies) maintained a Buy rating and lifted his price target to $454 from $424.

- Joseph Feldman (Telsey Advisory Group) maintained an Outperform rating and raised his price target to $435 from $410.

- Scot Ciccarelli (Truist Securities) maintained a Buy rating and raised his price target to $424 from $405.

- Steven Forbes (Guggenheim) reaffirmed a Buy rating and raised his price target to $425 from $400.

- Zachary Fadem (Wells Fargo) maintained an Overweight rating and raised his price target to $420 from $395.

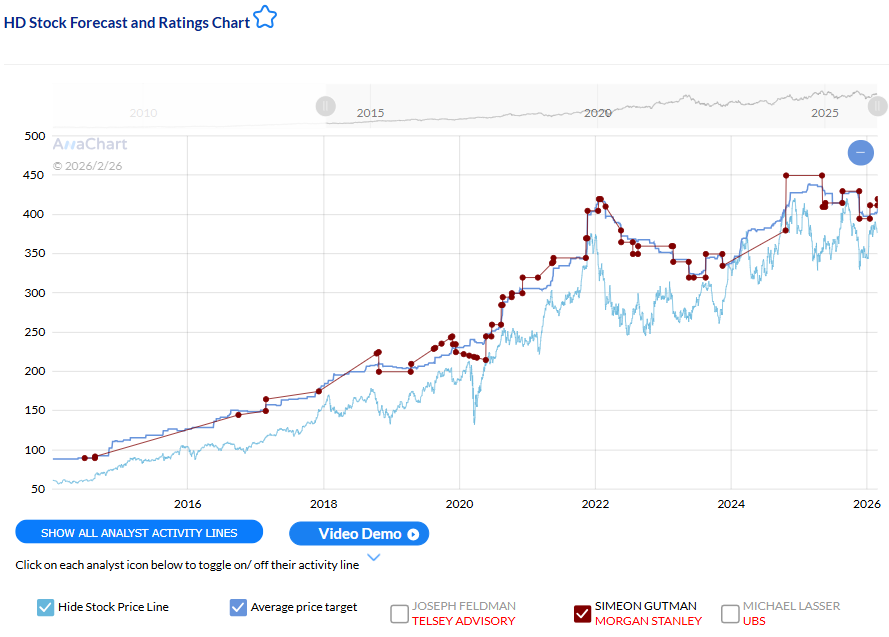

- Simeon Gutman (Morgan Stanley) maintained an Equal Weight rating and raised his price target to $420 from $412.

- Robert Ohmes (BofA Securities) maintained a Buy rating with a price target of $430.

- Zhihan Ma (Bernstein SocGen) maintained a Market Perform rating and raised his price target to $390 from $381.

Which Analyst Has the Current Best Track Record on HD?

Simeon Gutman of Morgan Stanley currently ranks among the top performers on HD, with an 88.89% price target hit ratio across 36 predictions and an average time to target of 346 days, reflecting consistent alignment between target setting and price realization.